2025-08-18

Steel companies' profits are expected to remain strong in August.

In the first half of 2025, facing the complex situation of increased external shocks and internal difficulties and challenges, China coordinated domestic economic work and international economic and trade struggles, effectively implemented more proactive and promising macro policies, and the national economy withstood the pressure and forged ahead. The overall economic operation was stable and improving, the decline in raw material prices led to a decline in costs, and driven by the rush to export effect, the profits of the steel industry continued to improve. According to data from the National Bureau of Statistics, from January to June 2025, the ferrous metal smelting and rolling processing industry achieved operating income of 3769.69 billion yuan, a year-on-year decrease of 7.5%; operating costs of 3580.64 billion yuan, a year-on-year decrease of 9.1%; and total profits of 46.28 billion yuan, a year-on-year increase of 1369.2%. In June, the ferrous metal smelting and rolling processing industry made a profit of 14.59 billion yuan, a decrease of 180 million yuan month-on-month and an increase of 2.18 billion yuan year-on-year.

In July, driven by the strong atmosphere of "anti-internal competition" in the industry, the enhanced expectation of the country to expand domestic demand, the safe and limited production of coking coal and coke, the landing of four rounds of coke market price increases, and the enhanced cost support, the domestic steel market showed a volatile rebound, and the profit margin of steel companies continued to expand. Looking forward to August, the steel industry will gradually shift from the off-season to the peak season. How will the operating conditions of steel companies evolve? The Lange Steel Research Center believes that the profitability of the steel industry will remain good in August 2025.

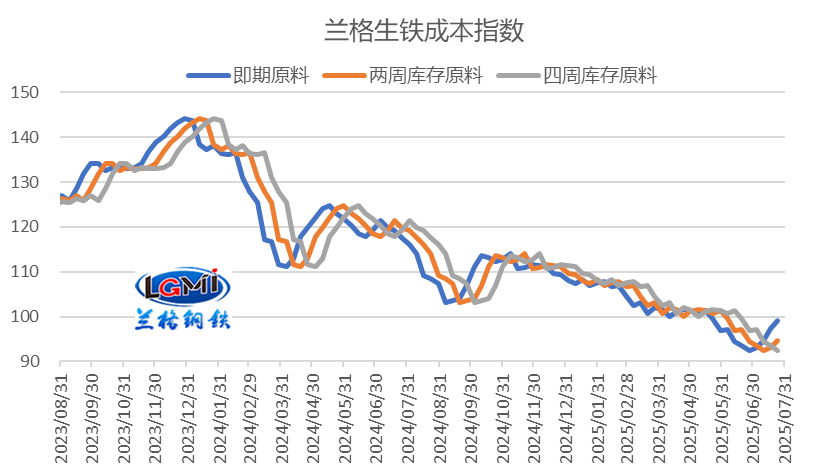

In July 2025, as raw material prices gradually increased, the immediate monthly average cost showed an upward trend. However, the monthly average cost calculated based on two-week and four-week inventory raw materials still declined. According to monitoring data from the Lange Steel Research Center, the raw material cost calculation pig iron cost index in July was 96.0, an increase of 1.8% compared with the same period last month; the two-week inventory raw material calculation pig iron cost index was 93.4, a decrease of 3.6% compared with the same period last month; the four-week inventory raw material calculation pig iron cost index was 94.3, a decrease of 5.3% compared with the same period last month, which shows that as raw material prices gradually increase, the shorter the inventory cycle, the higher the cost.

Figure 1 Trend Chart of Lange Pig Iron Cost Index

From the perspective of the average price of steel, the average Lange Steel Composite Steel Price Index in July was 3533 yuan (ton price, the same below), an increase of 2.6% compared with the previous month; among them, the average monthly price of rebar was 3327 yuan, an increase of 3.2% compared with the previous month; the average monthly price of hot-rolled coil was 3409 yuan, an increase of 3.8% compared with the previous month. From a cyclical perspective, there was a certain range of differences in cost in July due to changes in the raw material inventory cycle, but the increase in immediate costs was still less than the increase in steel prices, so the profit per ton of steel has improved.

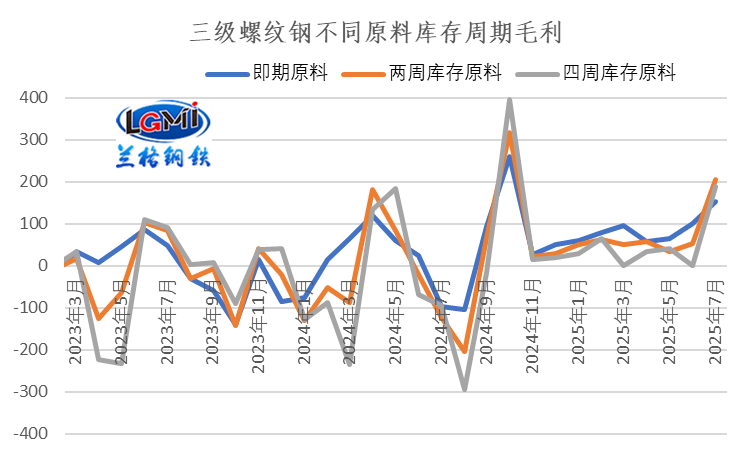

From the perspective of Grade 3 rebar, the calculated monthly average gross profit of Grade 3 rebar in July for immediate raw materials, two-week inventory raw materials, and four-week inventory raw materials were 154 yuan, 205 yuan, and 190 yuan, respectively, an increase of 52 yuan, 152 yuan, and 189 yuan compared with the previous month. The profitability of different raw material inventory cycles has improved, and the cost reduction under the four-week raw material inventory cycle is larger, and the profit improvement is more significant (see Figure 2 for details).

From the perspective of hot-rolled coil, the calculated gross profit of hot-rolled coil in July has also improved. The calculated profit of immediate raw materials was 88 yuan, an increase of 76 yuan compared with the previous month; the calculated monthly average profit of two-week and four-week inventory raw materials were 139 yuan and 124 yuan, respectively, both turning from loss to profit.

Figure 2 Changes in the Calculated Gross Profit Level of Grade 3 Rebar with Different Inventory Cycle Raw Materials

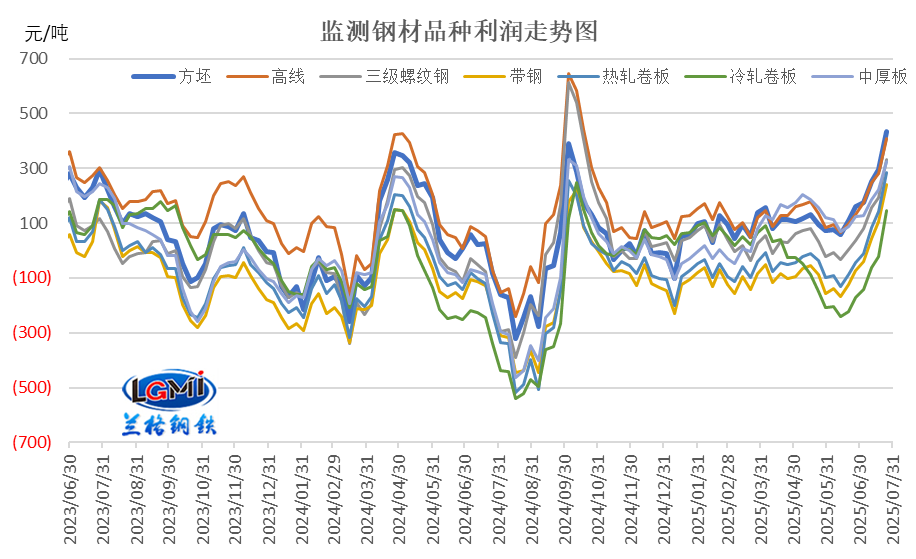

From the perspective of the gross profit performance of each variety calculated based on the four-week inventory raw materials, the gross profit of each variety calculated based on the four-week inventory raw materials in July showed a gradual upward trend, and the monthly profit of each variety increased; the monitoring data of the Lange Steel Research Center showed that among the monthly average gross profit of the seven monitored varieties, the gross profit of hot-rolled strip steel and hot-rolled coil increased the most, reaching 214 yuan and 213 yuan; the gross profit of medium and heavy plates increased the least, at 117 yuan; the increase in gross profit of other varieties was between 180-190 yuan.

Figure 3 Gross Profit Level of Main Steel Varieties (Four-Week Inventory Raw Materials)

In general, under the combined influence of the volatile rebound in the price of variety materials and the relatively small increase in production costs, the calculated gross profit per ton of steel for immediate, two-week, and four-week inventory raw materials of variety materials in July has improved; it is expected that the profit data of steel companies announced in July will still be relatively good.

The situation faced by the steel industry in August is still complex and volatile. From the perspective of the foreign environment, the global manufacturing PMI is showing a downward trend again, which means that the recovery momentum of global manufacturing is insufficient. The decline in the global manufacturing index has also led to a decline in the prosperity of China's manufacturing exports. China's manufacturing export order index has fallen back again in the contraction range, reflecting that China's manufacturing exports will still be under pressure in the later period.

From the perspective of the domestic environment, there are many unstable and uncertain factors in China, the domestic market is strong in supply and weak in demand, and some structural contradictions are still emerging. The foundation for economic recovery still needs to be consolidated. In the later period, China will maintain the continuity and stability of policies, enhance flexibility and foresight, focus on stabilizing employment, stabilizing enterprises, stabilizing the market, and stabilizing expectations, vigorously promote the domestic and international dual circulation, and promote the stable and healthy development of the economy.

From the perspective of the supply side of the steel industry, in August, with the air quality guarantee before major events, Beijing-Tianjin-Hebei and surrounding provinces may have some restrictions on production and construction, and it is expected that the daily output of crude steel will still decline.

From the demand side, in August, high temperature and heavy rainfall weather will gradually weaken, construction of construction projects will resume, and demand for construction steel will continue to rebound. The manufacturing industry is declining, and the new order and new export order index are falling back in the contraction range, and the demand for steel in the manufacturing industry may gradually be under pressure.

From the cost side, the average price of raw materials in July and August gradually increased, the production cost of steel gradually moved up, and the cost support for steel prices steadily increased.

In summary, the domestic steel market in August will still be affected by multiple factors. China's economy will focus on promoting the work of "strengthening domestic demand" and "stabilizing foreign trade", high temperature and heavy rainfall weather will change from strong to weak, the demand for construction steel market will change from off-season to peak season, and factors such as "anti-internal competition" and major events will keep the supply side at a relatively low level, the market supply and demand relationship is expected to improve, and the cost support is enhanced; Lange Steel Big Data AI-assisted decision-making system predicts that the domestic steel market in August may show a high level of volatility under the game of multiple long and short factors, and the average value will still move up compared with the previous month.

From the perspective of steel companies' profitability, the steel market in August 2025 will operate at a high level of volatility, and the average price of steel may still move up compared with the previous month. Under the situation of gradually increasing raw material costs, the Lange Steel Research Center expects that although there is a risk of gradually shrinking operating profits of steel companies from a high level in August, the overall profitability is expected to remain good. (Original article by Wang Guoqing of Lange Steel Research Center, please indicate the source for reprinting)

Previous Page

Previous Page

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com