2025-09-08

Lange Research: Initial Pressure of Steel Export Decline Emerges

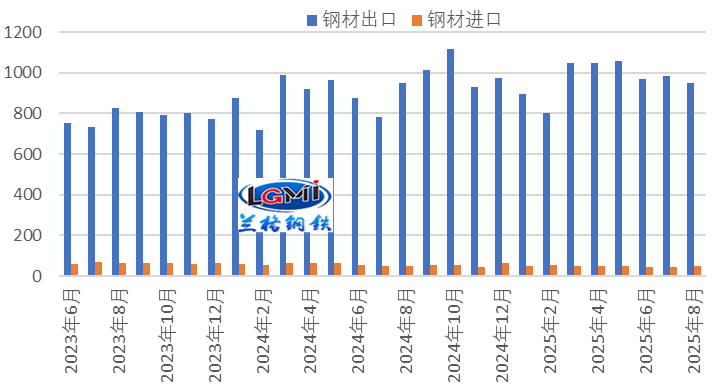

In August 2025, China's monthly steel exports showed a slight year-on-year increase. According to data from the General Administration of Customs, in terms of exports, in August, China exported 9.51 million tons of steel, a year-on-year increase of 0.1%, with the growth rate falling by 25.5 percentage points compared to the previous month; from January to August, China exported 77.49 million tons of steel, a year-on-year increase of 10.0%, with the growth rate falling by 1.4 percentage points compared to the previous month. In terms of imports, in August, China imported 0.5 million tons of steel, a year-on-year decrease of 2.0%, with the decline rate narrowing by 7.6 percentage points compared to the previous month; from January to August, China imported 3.977 million tons of steel, a year-on-year decrease of 14.1%, with the decline rate narrowing by 1.6 percentage points compared to the previous month.

Figure 1

Monthly Steel Import and Export Trends

In August 2025, China's steel exports showed a slight year-on-year increase (see Figure 1), but a month-on-month decline, decreasing by 326,000 tons compared to the previous month, a month-on-month drop of 3.3%. Although steel imports rebounded month-on-month and the year-on-year decline narrowed, imports remained at a low level. Therefore, in August, China's steel foreign trade still maintained a significant net export trend, but the year-on-year growth rate of net exports fell sharply. According to calculations by the Lange Steel Research Center, in August, China's net steel exports were 9.01 million tons, a year-on-year increase of 0.2%, with the growth rate falling by 27.8 percentage points compared to the previous month; from January to August, China's net steel exports were 73.513 million tons, a year-on-year increase of 11.5%, with the growth rate falling by 1.5 percentage points compared to the previous month.

Currently, China's steel exports still maintain a price advantage. The global manufacturing index has rebounded, and the external demand for manufacturing has slightly improved. The export order index of steel enterprises has risen to the expansion zone, which provides some short-term support for steel exports. However, global crude steel production has increased, and combined with trade frictions and related tariff increases, steel exports will still be restrained. Given the continued increase in the base of steel exports in the same period last year (10.15 million tons in September 2024), China's steel exports in September may face downward pressure year-on-year. The analysis of related influencing factors is as follows:

1. China's steel export price advantage still exists

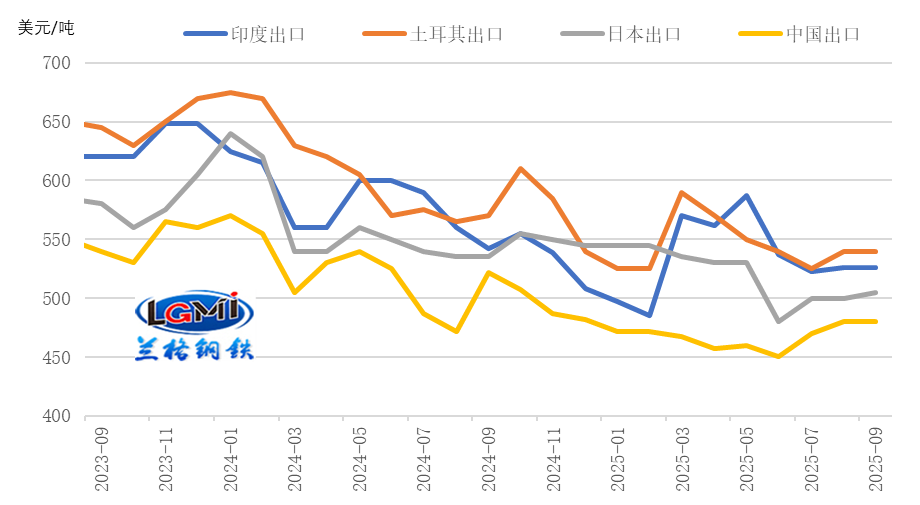

Currently, China's steel export price advantage still exists. According to monitoring data from the Lange Steel Research Center, as of September 8, 2025, the export prices (FOB) of hot-rolled coil from India, Turkey, and Japan were $525/ton, $540/ton, and $505/ton respectively, while China's hot-rolled coil export price (FOB) was $480/ton; currently, China's hot-rolled coil export prices are $45/ton, $60/ton, and $25/ton lower than those of India, Turkey, and Japan respectively (see Figure 2).

Figure 2

Monthly Export Price Comparison of Hot-Rolled Coil (FOB)

2. Overseas steel supply shifts from decline to increase, limiting China's steel export space

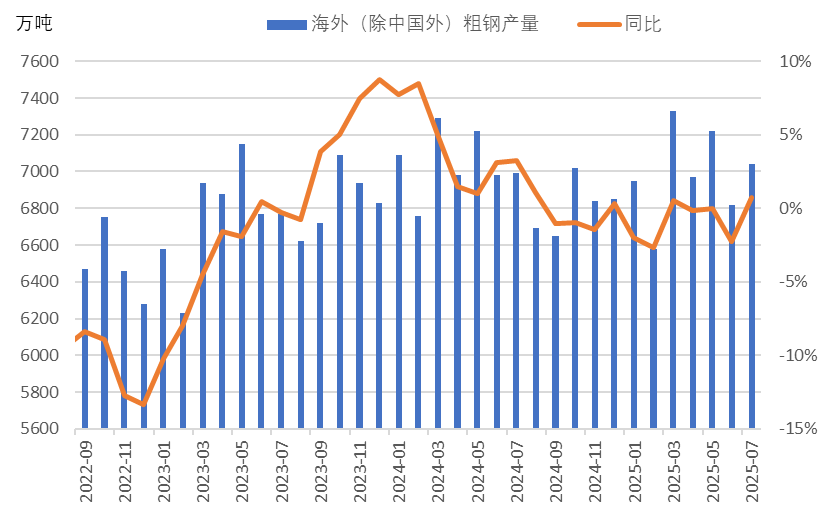

In July 2025, global crude steel production continued to show a year-on-year decline. In July, the crude steel output of 70 countries included in the World Steel Association statistics was 150.1 million tons, a year-on-year decrease of 1.3%. Looking at crude steel production outside China, it shifted from a decline to an increase year-on-year. Monitoring data from the Lange Steel Research Center shows that in July, production in other regions outside China was 70.4 million tons, a year-on-year increase of 0.7% (see Figure 3). The overseas supply shifted from decline to increase, somewhat limiting the external demand space for China's steel.

Figure 3

Monthly Crude Steel Production Outside China

3. Global manufacturing PMI has rebounded, and external demand sentiment has slightly improved

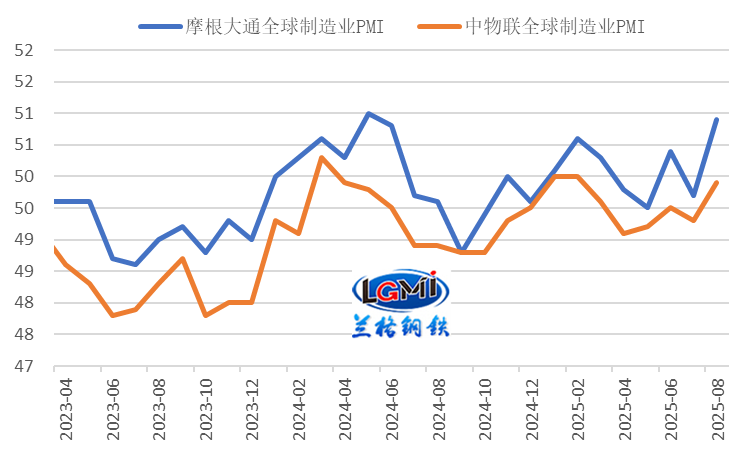

In August 2025, the global manufacturing index rebounded. According to the China Federation of Logistics and Purchasing, the global manufacturing PMI in August 2025 was 49.9% (see Figure 4), up 0.6 percentage points from the previous month. JPMorgan Chase's global manufacturing PMI in August rose from the contraction zone to the expansion zone, reaching 50.9%, an increase of 1.2 percentage points from the previous month. The global manufacturing index rebounded again, approaching or having returned to the expansion zone, indicating that the global manufacturing recovery strength has increased compared to the previous month, and the global economy is improving.

The rise in the global manufacturing index has also improved the external demand sentiment for China's manufacturing. According to the China Federation of Logistics and Purchasing and the National Bureau of Statistics Service Industry Survey Center, the Purchasing Managers' Index for China's manufacturing in August showed that the new export orders index was 47.2%, up 0.1 percentage points from the previous month. The export orders index rebounded again within the contraction zone, reflecting that the phased easing of China-US trade relations has somewhat stabilized market sentiment, and manufacturing export demand shows a trend of gradual stabilization.

Figure 4

Global Manufacturing PMI Performance (%)

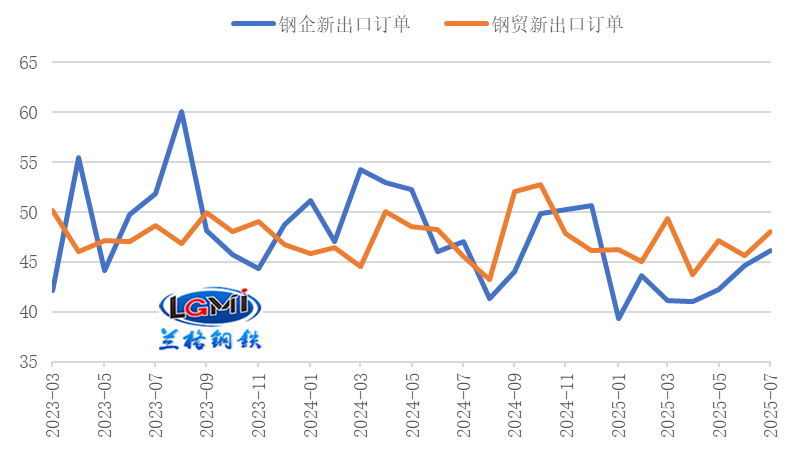

4. China's steel enterprises' export order index has risen to the expansion zone

Regarding steel export orders, China's steel enterprises' export order index continued to rise to the expansion zone; the China Federation of Logistics Steel Logistics Professional Committee surveyed that the new export orders index for steel enterprises in August 2025 was 50.4%, up 4.3 percentage points from the previous month (see Figure 5); the new export orders index for steel circulation enterprises surveyed by the China Metals Circulation Association & Lange Steel Network was 46.6%, down 1.5 percentage points from the previous month. The rise of the steel enterprises' export order index to the expansion zone will drive China's steel exports in the later period.

Figure 5

Changes in New Export Orders in the Steel Industry (%)

5. Global trade protection remains severe, continuing to suppress China's steel exports

Since August, trade frictions in the steel industry have continued. On August 13, Japan initiated an anti-dumping investigation on hot-dip galvanized steel strips and plates originating from China and South Korea; on September 1, Indonesia launched an anti-dumping investigation on hot-rolled coils of iron or non-alloy steel originating from China's Wuhan Iron and Steel Group Co., Ltd.; on September 4, Australia initiated anti-circumvention investigations on anti-dumping and countervailing cases involving welded pipes imported from mainland China, South Korea, Malaysia, and Taiwan, examining whether the products involved were exported to Australia through minor modifications to circumvent existing anti-dumping and countervailing measures. According to data from the China Trade Remedy Information Network, as of September 8, there have been 16 trade remedy investigation cases initiated by other countries and regions against China's steel industry this year, including 14 cases targeting China's steel products.

At the same time, early anti-dumping arbitration results are being released one after another. On August 5, the European Commission made a preliminary affirmative anti-dumping ruling on high-pressure seamless steel cylinders originating from China, with provisional anti-dumping duties ranging from 63.2% to 118.0%. On August 12, the South Korean Ministry of Strategy and Finance issued Announcement No. 2025-171, proposing a five-year anti-dumping duty of 21.62% on hot-rolled stainless steel sheets originating from China. On August 14, the Vietnamese Ministry of Industry and Trade issued Announcement No. 2310/QD-BCT, making a final affirmative anti-dumping ruling on coated carbon and alloy steel coils originating from China and South Korea, deciding to impose anti-dumping duties on the involved products, with China's rate ranging from 0% to 37.13%. On August 16, the Indian Ministry of Commerce and Industry announced a final affirmative safeguard measure ruling on imported non-alloy and alloy flat steel products, recommending safeguard duties for three years: 12% in the first year, 11.5% in the second year, and 11% in the third year. On August 14, the U.S. Department of Commerce announced a preliminary anti-dumping ruling on temporary steel fences imported from China, preliminarily determining dumping margins for Chinese producers/exporters at 136.57% to 187.69%, with a nationwide rate of 187.69% (adjusted to 187.69% after countervailing subsidy offsets). On August 29, the Brazilian Foreign Trade Committee Management Executive Committee (GECEX) issued Resolution No. 765 of 2025, making a final affirmative anti-dumping ruling on alloy or non-alloy tin-plated and chrome-plated steel coils of any width but less than 0.5 mm thickness originating from China, deciding to impose a five-year anti-dumping duty on the involved Chinese products, ranging from USD 284.34 to 499.35 per ton.

In summary, China's steel export price advantage still exists, and the steel enterprises' export order index has rebounded to the expansion range. However, the intensification of global trade protectionism will gradually suppress China's steel exports. Currently, China's steel exports to countries such as Vietnam, South Korea, India, and Brazil have shown a year-on-year decline trend. It is expected that steel export volume in September will still maintain a high level, but year-on-year pressure for decline may persist. (Original article by Wang Guoqing, Lange Steel Research Center; please indicate the source when reprinting.)

Previous Page

Previous Page

Rebar may rebound from the bottom

2025-09-09

Experts say city — September 9

2025-09-09

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com