2025-09-17

Improved credit conditions may spur the steel market to shift from "silver October" to "golden November."

Macroeconomic Data:

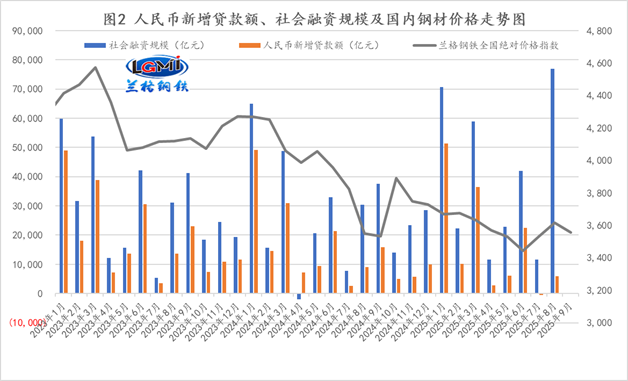

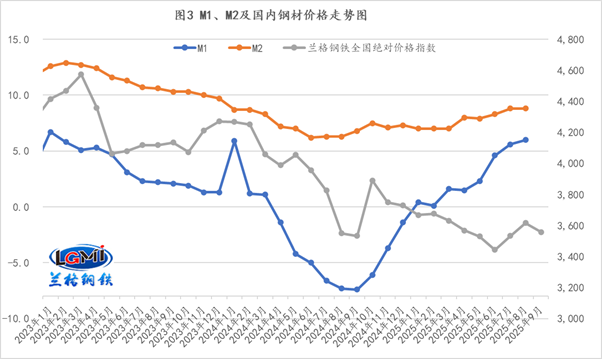

According to statistics from the People's Bank of China, as of the end of August 2025, the broad money supply (M2) stood at 331.98 trillion yuan, representing an 8.8% year-on-year increase. Meanwhile, the narrow money supply (M1) totaled 111.23 trillion yuan, up 6% compared to the same period last year. In the first eight months, RMB loans increased by 13.46 trillion yuan; and during the same period, the cumulative incremental size of social financing reached 26.56 trillion yuan, an increase of 4.66 trillion yuan over the same period last year.

(Lange Steel Research Center, Ge Xin, 15810671409 [WeChat account also available]; please credit the source when reprinting)

Lange's commentary:

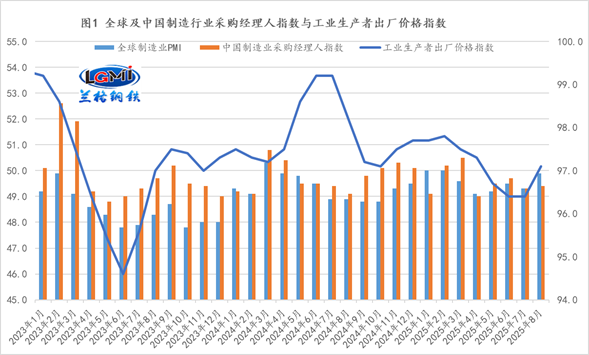

In August 2025, thanks to ongoing improvements in China's domestic market competition order—such as curbing disorderly competition and the orderly implementation of capacity management initiatives in key industries—the nationwide Producer Price Index (PPI) ended its eight-month consecutive decline on a month-on-month basis. However, compared with the same period last year, PPI still fell by 2.9%, though the decline narrowed by 0.7 percentage points from the previous month (see Figure 1 for details). Currently, the combined effects of policies aimed at expanding domestic demand and combating "involution" are beginning to show initial results. Nevertheless, it remains crucial to significantly strengthen macroeconomic policies that counter-cyclically adjust the economy, thereby further boosting the sustained release of steel demand in manufacturing sectors.

Looking at the financial data from January to August, credit and social financing both showed a year-on-year rebound. Notably, the increase in new RMB loans was significantly lower compared to the same period last year; meanwhile, the incremental scale of social financing saw a substantial year-on-year rise (see Figure 2 for details). Meanwhile, narrow money (M1) has maintained positive year-on-year growth for eight consecutive months, with the growth rate continuing to accelerate, while broad money (M2) has remained relatively stable on a year-on-year basis (see Figure 3 for details).

From the lending perspective, corporate loans increased by 12.22 trillion yuan from January to August, including a rise of 3.82 trillion yuan in short-term loans and 7.38 trillion yuan in medium- and long-term loans, along with an increase of 877.8 billion yuan in bill financing. This indicates that businesses are shifting from a weaker to a stronger willingness to invest in both the short and long term, while their appetite for short-term risk management continues to wane. Meanwhile, household loans grew by 711 billion yuan during the same period, yet this included a decline of 372.5 billion yuan in short-term loans and a rise of 1.08 trillion yuan in medium- and long-term loans—suggesting that overall demand for household borrowing remains insufficient.

From the perspective of social financing, from January to August, the incremental scale of social financing reached 26.56 trillion yuan, an increase of 4.66 trillion yuan compared to the same period last year. Among them, RMB loans extended to the real economy rose by 12.93 trillion yuan, although this marked a year-on-year decrease of 485.1 billion yuan. Meanwhile, net corporate bond financing stood at 1.56 trillion yuan, down 221.4 billion yuan from the previous year. In contrast, net government bond financing surged to 10.27 trillion yuan, representing a significant year-on-year increase of 4.63 trillion yuan—indicating that the government has stepped up its efforts in net bond issuance, while corporate entities continue to show limited appetite for borrowing.

Currently, China's macro policies are working in synergy, leading to generally stable performance in the national economy. Transformation and upgrading continue to advance steadily, yielding new achievements in high-quality development. However, we must also recognize that the external environment remains complex and challenging, marked by numerous uncertainties and instabilities. Meanwhile, domestic market conditions show strong supply but weak demand, creating operational difficulties for some enterprises. Looking ahead, we must adhere to the overarching principle of pursuing progress while maintaining stability, fully, accurately, and comprehensively implementing the new development philosophy. We will accelerate the establishment of a new development paradigm, rigorously implement and refine all macroeconomic policies, and focus on stabilizing employment, businesses, markets, and expectations. At the same time, we will strengthen macro policy adjustments, effectively unlock domestic demand potential, deepen reform, opening-up, and innovation, bolster the robust domestic economic loop, foster seamless domestic-international circulation, and drive steady, healthy economic growth.

Currently, the domestic steel market is at a critical "turning point" as it transitions between the off-season and peak season. However, economic data reveal that downstream demand remains less than optimistic. Infrastructure investment, which has traditionally provided solid support for construction steel demand, is now showing significantly weaker traction, while real estate investment continues to weigh heavily on the market. Meanwhile, industries that previously underpinned demand for manufacturing steel are also beginning to show signs of weakening. Moreover, given that the operational dynamics of the domestic steel market this year have left limited room for speculative activities, the prevailing market sentiment still largely follows the logic of "expectations in the off-season, reality in the peak season." Meanwhile, the Federal Reserve is set to hold its monetary policy meeting on September 16 and 17. Market expectations widely anticipate that the Fed will initiate a new round of interest rate cuts during this meeting. Such a move could once again pave the way for China's central bank to adjust its own interest rates, helping strike a delicate balance between short-term and long-term goals, sustaining growth while managing risks, and maintaining equilibrium both domestically and internationally. This development has also bolstered market confidence in the possibility of further proactive macroeconomic policy actions—potentially injecting fresh momentum into what has historically been a traditionally strong "Golden September," despite the current subdued market conditions. (Lange Steel Research Center, Ge Xin, 15810671409 [WeChat account also available]; please credit the source when reprinting.)

Experts say city — September 15

2025-09-15

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com