2026-01-12

Steel companies’ profitability may improve at the start of 2026.

In 2025, the steel industry as a whole is expected to maintain a relatively stable operating environment. According to data from the National Bureau of Statistics, from January to November 2025, the ferrous metal smelting and rolling processing industry achieved operating revenue of 7,064.8 billion yuan, down 4.1% year-on-year; operating costs totaled 6,672.47 billion yuan, down 5.6% year-on-year; and total profits reached 111.5 billion yuan, up 1,752.2% year-on-year. In November alone, the ferrous metal smelting and rolling processing industry reported profits of 6.18 billion yuan, a decrease of 1.8 billion yuan from the previous month and a drop of 80.2% year-on-year.

In December 2025, influenced by a confluence of factors—including a relatively stable global economic recovery, continued weak performance in domestic economic indicators, a still-divergent pattern of industry supply release, the onset of the traditional off-season for market demand, and strong resilience in cost support—China’s steel market is experiencing a range-bound, volatile trend. Persistent strength in costs continues to squeeze the profit margins of steel enterprises, and the industry’s profitability level has further narrowed compared to November.

Looking ahead to January 2026, although the steel industry will still be in the off-season for demand, positive factors are gradually emerging, including increasingly clear signals of policy support, differentiated adjustments in raw material costs, and continued strong regulatory measures on the supply side. According to the Lange Steel Research Center, the steel industry’s profit margins are expected to improve in January 2026. However, the extent of this improvement will still be constrained by factors such as the pace of demand recovery and fluctuations in costs, resulting in an overall trend characterized by “weak recovery and gradual improvement.”

In December 2025, the raw material market showed signs of structural adjustment. Iron ore prices gradually stabilized, while coking coal prices continued to decline, leading to diverging trends in raw material costs across different inventory cycles. According to monitoring data from the Lange Steel Research Center, the spot raw material-based pig iron cost index for December was 106.6, down 1.4% from the same period last month. The two-week inventory-based pig iron cost index stood at 108.3, up 1.5% from the same period last month, and the four-week inventory-based pig iron cost index reached 108.1, up 2.5% from the same period last month—further highlighting the widening cost differences across various inventory cycles.

Figure 1: Trend Chart of the Langer Pig Iron Cost Index

Looking at steel price performance, the average monthly value of Lange Steel’s comprehensive steel price index in December 2025 was 3,515 yuan/ton, up slightly by 0.4% from the previous month, indicating a modest upward shift in the price center. By specific product category, the average monthly price of rebar was 3,323 yuan/ton, up 1.7% from the previous month, showing relatively strong performance; the average monthly price of hot-rolled coil was 3,358 yuan/ton, down slightly by 0.4% from the previous month, exhibiting a narrow-range fluctuating trend. On the cost side, in December, costs under different raw material inventory cycles showed divergent trends, with fluctuations ranging from -1.4% to 2.5%. Meanwhile, steel prices fluctuated between -0.4% and 1.7%. The pace of cost and steel price movements was not entirely synchronized, further contributing to continued divergence in the profitability per ton of steel across various product categories.

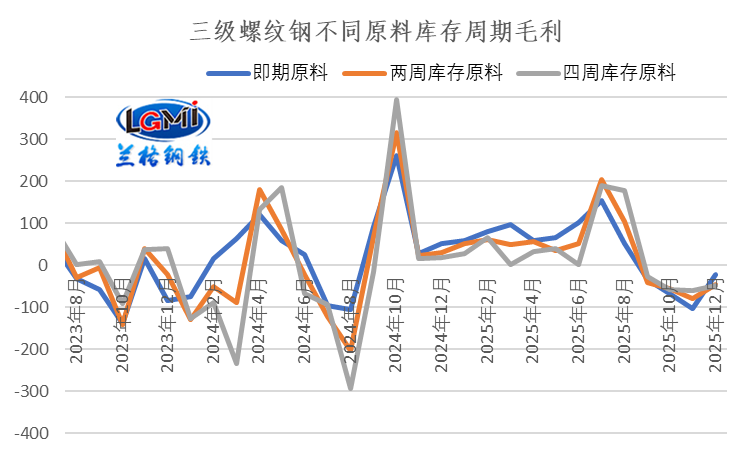

Looking at the profitability performance of Grade-3 rebar, its profit situation in December 2025 showed an improvement compared to the previous month, with gross profits per ton of steel declining less across different raw-material inventory cycles. Specifically, the monthly average gross profit calculated based on spot raw materials was -21 yuan/ton, a reduction in loss of 81 yuan/ton from the previous month; the monthly average gross profit calculated based on two-week inventory of raw materials was -45 yuan/ton, a reduction in loss of 35 yuan/ton from the previous month; and the monthly average gross profit calculated based on four-week inventory of raw materials was -49 yuan/ton, a reduction in loss of 10 yuan/ton from the previous month. As a result, the industry’s profit pressure has eased somewhat (see Figure 2 for details).

From the perspective of profit performance for hot-rolled coil, December 2025 showed a structurally divergent trend in profitability. Specifically, the calculated monthly average gross profit based on spot raw materials was -149 yuan/ton, a reduction in loss of 19 yuan/ton compared to the previous month, thanks to the support from declining spot raw material costs, which led to an improvement in profitability. However, affected by rising costs of two-week and four-week inventory raw materials, the corresponding calculated gross profits were -173 yuan/ton and -177 yuan/ton, respectively, representing increases in loss of 28 yuan/ton and 53 yuan/ton compared to the previous month. Under the medium- and long-term inventory cycle, profit pressure has further intensified, resulting in an overall mixed profit performance.

Figure 2: Changes in Gross Profit Levels for Raw Materials Calculated Across Different Inventory Cycles of Grade III Rebar

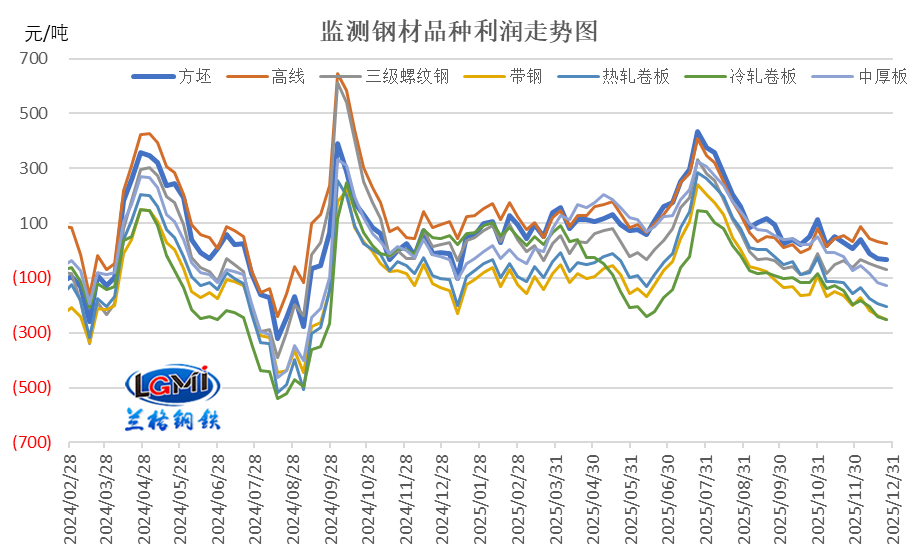

Judging from the gross profit performance of various steel products calculated based on raw material inventories across different regions, December 2025 is expected to show an overall volatile trend—first rising and then falling. Significant differentiation in profitability has emerged among different product categories: while profits for construction materials showed a slight improvement, profits for other product categories continued to weaken. According to monitoring data from the Lange Steel Research Center, among the seven major steel products included in the survey, the average monthly gross profit for high-line steel and rebar improved compared to the previous month, with the improvement ranging from 9 to 12 yuan per ton. Meanwhile, the average monthly gross profit for all other product categories declined, with the decline ranging from 36 to 70 yuan per ton, further highlighting the widening gap in profitability among different product types.

Figure 3: Gross Profit Margins for Major Steel Products (Raw Materials in Inventory Around the Perimeter)

Overall, under the combined impact of dual divergence—between steel product prices and production costs—by December 2025, the gross profit per ton of various steel products will show a markedly differentiated pattern when calculated based on spot, two-week, and four-week inventory levels. It is expected that the steel enterprise profit data for December 2025, as released by the National Bureau of Statistics, will exhibit an even narrower range of fluctuations compared to the previous month, signaling that the industry’s profitability is gradually entering a bottoming-out phase.

In January 2026, the steel industry will continue to face a complex and ever-changing development environment. From the perspective of the domestic macroeconomic environment, structural contradictions—such as strong supply and weak demand—remain prominent in economic operations. Consumer willingness to spend remains cautious, and investment vitality remains insufficient. With domestic demand growth momentum yet to be fully unleashed, the economy is currently at a critical stage of transformation, striving for steady progress while enhancing quality and efficiency. Coupled with the complex and severe external environment and profound adjustments in the global landscape, the steel industry continues to face significant uncertainties in its operation and development.

From the supply side of the steel industry, steel mills continue to expand the scope of maintenance and production cuts, squeezed by both a significant weakening in end-demand and deepening losses in certain steel product categories. Coupled with the continued implementation of autumn and winter environmental production restrictions in some regions, expectations of supply contraction have become even clearer. As a result, domestic steel production is expected to remain at low levels. According to estimates from the Lange Steel Research Center, the nation’s daily crude steel output in December 2025 may stabilize around 2.3 million tons. From the perspective of traditional seasonal patterns, daily crude steel output in January 2026 is likely to show a month-on-month rebound; however, the magnitude of this rebound will be constrained by demand.

From the demand side, as the winter climate in both northern and southern regions deepens further in January 2026, the steel market will officially enter the traditional off-season for demand. Construction site activities will gradually become more restricted, and demand for construction steel will continue its seasonal weakening trend, facing certain downward pressures both month-on-month and year-on-year. Meanwhile, steel demand from the manufacturing sector, benefiting from the industry’s resilience, is likely to maintain a steady pace of release, with the differentiation in demand structure becoming even more pronounced.

From the cost perspective, the substantial decline in the average price of coke in December 2025 has driven down the monthly average production costs in the steel industry, thereby weakening the cost support for steel prices. At the beginning of January 2026, a new round of coke price reductions took effect, further prompting a slight decrease in steel companies' production costs and creating some room for profit recovery.

Overall, in January 2026, the domestic steel market will continue to be influenced by a complex interplay of multiple factors: On the policy front, both favorable measures and constraints coexist. The policies outlined at the Central Economic Work Conference—“expanding domestic demand, combating involution, and stabilizing the real estate sector”—are entering a phase of substantive implementation. Meanwhile, starting January 1, the new policy on steel export licenses will officially take effect, and the European Union’s Carbon Border Adjustment Mechanism (CBAM) will fully come into force. Market expectations are diverging amid policy guidance and the reshaping of international rules. On the demand side, seasonal factors are weighing on construction steel demand, which continues to weaken, while steel demand from the manufacturing sector remains resilient, further accentuating structural differentiation. On the supply side, constrained by dual factors—environmental production restrictions and scheduled maintenance at steel mills—capacity release is limited, and the market supply-demand balance is likely to remain in a “weak equilibrium” state. According to forecasts from Lange Steel Big Data’s AI-assisted decision-making system, the domestic steel market in January 2026 is expected to exhibit a volatile yet relatively strong performance.

From the perspective of steel companies’ profitability, thanks to the dual support of a relatively strong and volatile steel market starting from January 2026 and declining raw material costs, the Lange Steel Research Center expects the industry’s profit margins to improve somewhat. However, it is important to note that constraints such as high and volatile iron ore prices, weak end-demand, and shrinking exports remain unresolved. As a result, steel companies’ profits are unlikely to see a substantial rebound in the short term, and the overall trend will be characterized by “weak recovery and gradual improvement.” (Original article by Wang Guoqing, Lange Steel Research Center; please indicate the source when reprinting.)

2026-01-26

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com