2025-01-14

In 2025, China's steel exports will face some pressure.

In December 2024, China's monthly steel exports showed a growth trend both month-on-month and year-on-year. According to statistics from the General Administration of Customs, in December 2024, China exported 9.727 million tons of steel, a year-on-year increase of 25.9%; from January to December, China exported 110.716 million tons of steel, a year-on-year increase of 22.7%. In terms of imports, in December, China imported 621,000 tons of steel, a year-on-year decrease of 6.6%; from January to December, China imported 6.815 million tons of steel, a year-on-year decrease of 10.9% (see Figure 1).

Figure 1 Monthly Steel Import and Export Trends

In December 2024, China's steel exports still showed a significant year-on-year growth trend; month-on-month, the export volume increased by 447,000 tons compared to November, a month-on-month increase of 4.8%; although steel imports in December increased by 32.1% month-on-month, they remained at a low level, thus maintaining a significant net export situation in China's steel foreign trade in December. According to calculations from the Lange Steel Research Center, in December 2024, China's net steel exports were 9.106 million tons, a year-on-year increase of 28.9%, with a growth rate rebounding by 9.7 percentage points compared to the previous month; from January to December 2024, China's net steel exports were 103.901 million tons, a year-on-year increase of 25.8%.

Currently, China's steel export price advantage still exists; overseas steel supply continues to decline year-on-year; at the same time, the global manufacturing index is fluctuating slightly in the contraction zone, and "grabbing exports" is driving a weak recovery in external demand; China's steel enterprises' export order index continues to rise in the expansion zone, coupled with the depreciation of the RMB, steel export competitiveness remains strong; in the future, trade frictions and preliminary rulings will gradually emerge, and the suppression on steel exports will gradually become apparent. Given the low base in January and February of the previous year, China's steel exports may still maintain a year-on-year growth trend in January and February 2025, but in March, as the base increases, there may be pressure for a year-on-year decline. The analysis of related influencing factors is as follows:

1. China's steel export price advantage still exists

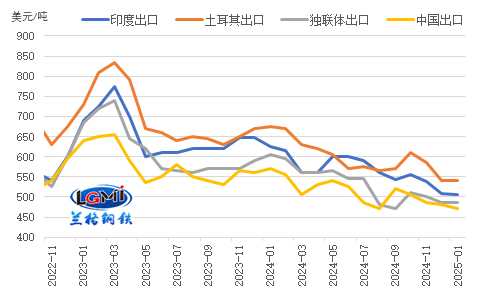

With the fluctuation and adjustment of domestic and foreign steel prices, China's steel export price advantage still exists. According to monitoring data from the Lange Steel Research Center, as of January 10, 2025, the export prices (FOB) of hot-rolled coils from India, Turkey, and the CIS were $507/ton, $540/ton, and $485/ton respectively, while China's hot-rolled coil export price (FOB) was $472/ton; currently, China's hot-rolled coil export prices are $35/ton, $68/ton, and $13/ton lower than those of India, Turkey, and the CIS respectively (see Figure 2). The price advantage of steel exports still provides certain support for our future exports.

Figure 2 Monthly Export Price Comparison of Hot-Rolled Coils (FOB)

2. Global manufacturing PMI fluctuates in the contraction zone, with weak recovery in external demand

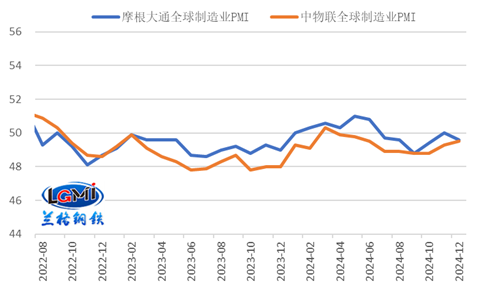

In December 2024, the global manufacturing index continued to show a fluctuating trend in the contraction zone. According to the China Federation of Logistics and Purchasing, the global manufacturing PMI in December 2024 was 49.5% (see Figure 3), an increase of 0.2 percentage points from the previous month, reaching a new high since the second half of 2024. JPMorgan's global manufacturing PMI in December fell back to 49.6% in the contraction zone, a decrease of 0.4 percentage points from the previous month, again falling back into the contraction zone. The recovery momentum of the global economy still appears insufficient.

Figure 3 Global Manufacturing PMI Performance (%)

From the data released by the China Federation of Logistics and Purchasing and the National Bureau of Statistics Service Industry Survey Center for December 2024, China's manufacturing new export orders index was 48.3%, an increase of 0.2 percentage points from the previous month, continuing to rise in the contraction zone, reflecting that the expectation of rising trade protectionism has led to a short-term "grabbing exports" driving the weak recovery of overseas demand for Chinese manufacturing.

3. The year-on-year decline in overseas steel supply has expanded, continuing to release space for China's steel exports

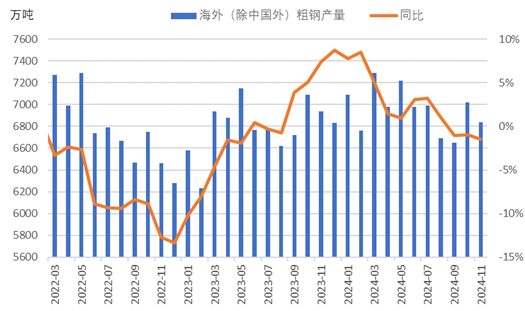

In November 2024, global crude steel production showed a year-on-year growth trend. In November 2024, the crude steel production of 71 countries included in the World Steel Association statistics was 146.8 million tons, a year-on-year increase of 0.8%. Excluding China, the crude steel production in other regions continued to decline year-on-year. According to monitoring data from the Lange Steel Research Center, in November, the production outside China was 68.4 million tons, a year-on-year decrease of 1.4%, with the decline expanding by 0.4 percentage points compared to the previous month (see Figure 4). The decline in overseas supply continues to release space for China's steel external demand.

Figure 4 Monthly Crude Steel Production Situation Overseas (Excluding China)

4. The export order index of China's steel enterprises continues to rise in the expansion zone

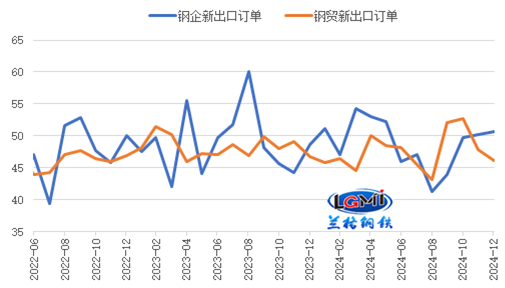

In terms of export orders, the export order index of China's steel enterprises continues to rise in the expansion zone; the new export order index for steel enterprises surveyed by the China Federation of Logistics and Purchasing in December 2024 was 50.6%, an increase of 0.4 percentage points from the previous month (see Figure 5); the new export order index for steel circulation enterprises surveyed by the China Gold Association & Lange Steel Network was 46.1%, a decrease of 1.7 percentage points from the previous month. The export order index of steel enterprises continues to rise in the expansion zone, providing certain support for China's future steel exports.

Figure 5 Changes in New Export Orders in the Steel Industry (%)

5. The short-term depreciation of the RMB continues to enhance the competitiveness of steel exports

Since December 2024, the RMB exchange rate against the US dollar has continued to decline from a high level. As of the close on January 8, 2025, the onshore RMB against the US dollar has cumulatively fallen by 994 basis points since the end of November, reported at 7.3326, a decrease of about 1.4%. Currently, the market's expectations regarding Trump's tariff policies, which may push up inflation, have kept the US dollar strong, with the dollar index rising continuously, leading to a continued depreciation of the RMB. The continued depreciation of the RMB continues to enhance the competitiveness of China's steel exports.

6. Trade frictions in the steel industry continue, which will suppress China's steel exports in the future

Since 2024, as China's steel export volume remains high, the number of trade frictions faced by the steel industry has significantly increased. In addition to Europe and the United States, countries in Southeast Asia, South America, Oceania, and Africa have increasingly imposed trade sanctions on China's steel exports. According to tracking data from the Lange Steel Research Center, in 2024, China's exported steel products and steel products encountered 41 trade remedy investigations initiated by 18 countries and regions, including 27 anti-dumping investigations, 7 combined anti-dumping and countervailing investigations, 3 circumvention investigations, 1 transitional review investigation, and 3 safeguard investigations; compared to 2023, the number of countries increased by 5, and the number of cases increased by 20.

As global trade protectionism intensifies in 2025, overseas tariff rulings and enforcement will further restrict China's steel exports. At the beginning of 2025, Thailand initiated a circumvention investigation against China's special iron pipes and steel pipes anti-dumping case, and South Africa initiated a safeguard investigation against imported steel flat-rolled products. Indonesia continues to impose anti-dumping duties on hot-rolled sheets involving China. The impact of intensified trade protectionism on China's steel exports will gradually manifest in 2025, and it is expected that China's steel exports, including both direct and indirect exports, will face certain pressure.

In summary, the current advantages of China's steel export prices still exist, the depreciation of the RMB, and the recovery of export orders from steel companies all provide certain support for exports. However, the momentum of trade friction remains unabated. Based on the low export base of steel in January-February 2024 (an average of 7.955 million tons per month), steel exports in January-February 2025 are still expected to maintain growth year-on-year. However, in March, as the base increases, there may be downward pressure year-on-year. Looking at the whole year of 2025, with the intensification of global trade protectionism, overseas tariff rulings and enforcement will further restrict China's steel exports. The Lange Steel Research Center predicts that China's steel export volume will face some pressure in 2025 but will still remain relatively high, with an expected annual steel export volume of around 80-100 million tons, shifting from an increase to a decrease year-on-year.

Experts say the market - January 20

2025-01-20

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com