2025-01-15

The "moderately loose" monetary policy will provide support for the steel market's "winter storage."

Macroeconomic Data:

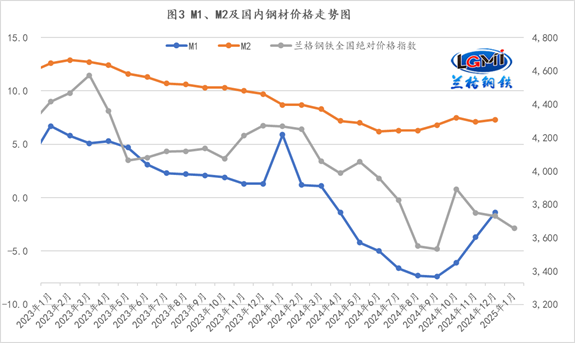

According to statistics from the People's Bank of China, by the end of December 2024, the balance of broad money (M2) was 313.53 trillion yuan, a year-on-year increase of 7.3%. The balance of narrow money (M1) was 67.1 trillion yuan, a year-on-year decrease of 1.4%. In 2024, new RMB loans increased by 18.09 trillion yuan; the cumulative increase in the scale of social financing in 2024 was 32.26 trillion yuan, which is 3.32 trillion yuan less than the previous year.

Langge Commentary:

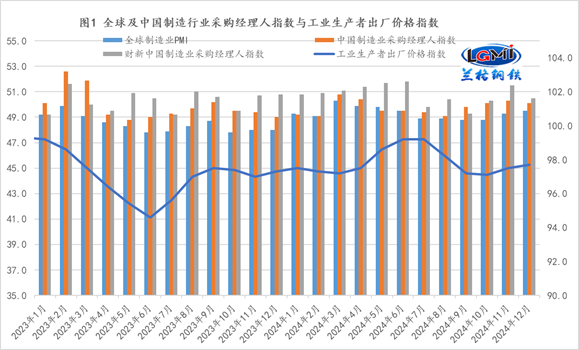

In December 2024, affected by factors such as some industries entering the traditional off-season for production and fluctuations in international commodity prices, the national PPI decreased by 0.1% month-on-month and by 2.3% year-on-year, with the year-on-year decline narrowing by 0.2 percentage points compared to the previous month (see Figure 1). Currently, the Chinese economy continues to show signs of recovery, but it faces significant pressure. Although there are signs of demand recovery, the overall imbalance of supply exceeding demand remains serious, and the release of demand for steel in manufacturing is still insufficient in the short term.

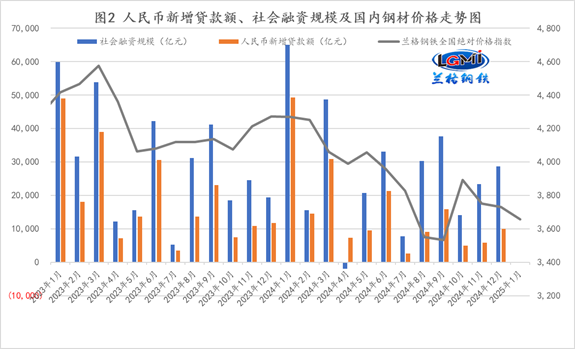

From the financial data of 2024, both credit and social financing show a downward trend, with the new RMB loan amount significantly lower year-on-year; the increase in the scale of social financing is also lower year-on-year (see Figure 2); although narrow money (M1) has experienced negative growth for nine consecutive months, the rate of decline continues to narrow, while the year-on-year growth rate of broad money (M2) has slightly rebounded (see Figure 3).

From the loan side, in 2024, corporate loans increased by 17.91 trillion yuan, of which short-term loans increased by 3.92 trillion yuan, medium and long-term loans increased by 13.57 trillion yuan, and bill financing increased by 341 billion yuan, indicating that corporate willingness to invest in both short-term and medium-long term has significantly strengthened, and the pace of risk control has weakened. In 2024, household loans increased by 4.33 trillion yuan, of which short-term loans increased by 1.78 trillion yuan, and medium and long-term loans increased by 2.55 trillion yuan, indicating that as China's loan interest rates steadily decline, household confidence is continuously recovering.

From the social financing side, the cumulative increase in the scale of social financing in 2024 was 32.26 trillion yuan, which is 3.32 trillion yuan less than the previous year. Among them, RMB loans issued to the real economy increased by 17.05 trillion yuan, a year-on-year decrease of 5.17 trillion yuan; net financing of corporate bonds was 1.91 trillion yuan, a year-on-year increase of 283.9 billion yuan; net financing of government bonds was 11.3 trillion yuan, a year-on-year increase of 1.69 trillion yuan, indicating that net financing of government bonds remains the main force, while corporate financing willingness has increased.

In 2025, China's economy should adhere to the principle of seeking progress while maintaining stability, promoting stability through progress, maintaining integrity and innovation, establishing first and then breaking, system integration, and collaborative cooperation. It should implement a more proactive fiscal policy and moderately loose monetary policy, enrich and improve the policy toolbox, strengthen extraordinary counter-cyclical adjustments, and effectively implement a policy "combination punch." From the perspective of the central bank, in 2025, it should implement a moderately loose monetary policy, prevent and resolve financial risks in key areas, further deepen financial reform and high-level opening up, focus on expanding domestic demand, stabilizing expectations, and stimulating vitality, creating a good monetary and financial environment for promoting sustained economic recovery; it should comprehensively use various monetary policy tools, adjust the reserve requirement ratio and interest rates at the right time based on domestic and international economic and financial conditions and financial market operations, maintain ample liquidity, and ensure stable growth of the total financial volume, aligning the growth of social financing scale and money supply with economic growth and price level expectations; it should scientifically use structural monetary policy tools, optimize the tool system, strengthen coordination with fiscal policy, and further increase financial support for technological innovation and consumption; it should continue to effectively address the debt risk resolution of local government financing platforms; it should improve and strengthen macro-prudential management of real estate finance, supporting the construction of a new model for real estate development; it should make good use of the two structural monetary policy tools that support the capital market, explore normalized institutional arrangements, and maintain the stable operation of the capital market.

Currently, the domestic steel market will be affected by multiple factors such as continuous external disturbances, strong expectations for economic policies at the beginning of the year, stable and strong fluctuations in steel mill supply, intensified winter storage competition, and weakened cost support. As the Spring Festival holiday approaches, the domestic steel market will gradually promote traditional winter storage operations in the process of the game between strong policy expectations and weak seasonal realities. However, given the significant increase in external uncertainty and instability, this year's winter storage faces considerable operational difficulties in both price and scale.(Langge Steel Research Center, Ge Xin, 15810671409 (WeChat same number) Please indicate the source when reprinting)

Previous Page

Experts say the market - January 20

2025-01-20

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com