2025-06-09

Steel exports are expected to see their sixth consecutive year-on-year increase

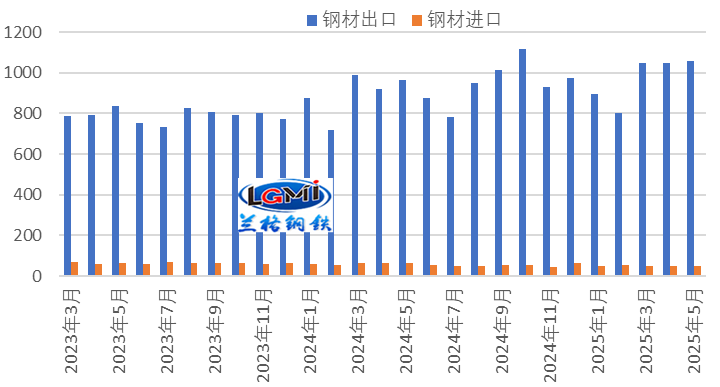

In May 2025, China's monthly steel exports continued to show year-on-year growth. According to the General Administration of Customs statistics, in terms of exports, in May, China exported 10.578 million tons of steel, a year-on-year increase of 9.8%; from January to May, China exported 48.469 million tons of steel, a year-on-year increase of 8.9%. In terms of imports, in May, China imported 481,000 tons of steel, a year-on-year decrease of 24.8%; from January to May, China imported 2.553 million tons of steel, a year-on-year decrease of 16.1%.

Figure 1: Monthly Trend of Steel Imports and Exports

In May 2025, China's steel exports continued to show year-on-year growth (see Figure 1), while steel imports remained at a low level. Therefore, China maintained a significant net export trend in steel foreign trade in May. Data calculated by Lange Steel Research Center shows that in May, China's net steel exports were 10.097 million tons, a year-on-year increase of 12.3%, with the growth rate falling by 3.8 percentage points from the previous month; from January to May, China's net steel exports were 45.916 million tons, a year-on-year increase of 10.3%, with the growth rate rising by 0.5 percentage points from the previous month.

Currently, China still has a price advantage in steel exports; overseas steel supply has turned from increasing to decreasing year-on-year, releasing some space for steel exports; however, the global manufacturing PMI is still in the contraction range, and external demand remains weak. The export order index of China's steel industry has rebounded slightly in the contraction range, and the trade frictions faced by the steel industry are still ongoing, and the inhibitory effect on steel exports will gradually become apparent. It is expected that China's steel exports will remain relatively high in June, and given the low base of steel exports in the same period last year (8.74 million tons), steel exports in June may still maintain year-on-year growth. The following is an analysis of the relevant influencing factors:

1. China's Steel Export Price Advantage Remains

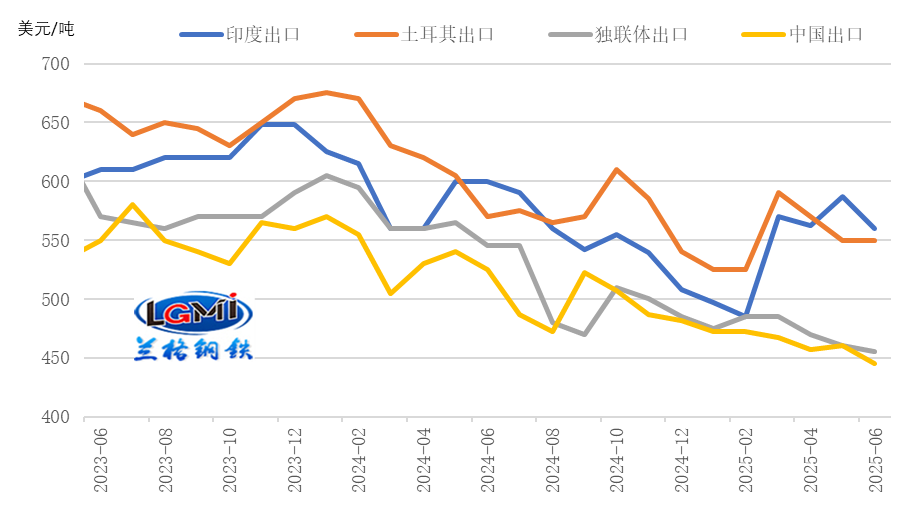

Currently, China still maintains a price advantage in steel exports. Data monitored by Lange Steel Research Center shows that as of June 6, 2025, the FOB export prices of hot-rolled coils in India, Turkey, and the Commonwealth of Independent States were US$560/ton, US$550/ton, and US$455/ton respectively, while China's FOB export price of hot-rolled coils was US$445/ton; currently, China's hot-rolled coil export prices are US$115/ton, US$105/ton, and US$10/ton lower than those in India, Turkey, and the Commonwealth of Independent States respectively (see Figure 2).

Figure 2: Comparison of Monthly Export Prices (FOB) of Hot-Rolled Coils

2. Overseas Steel Supply Has Decreased Year-on-Year, Slightly Releasing Export Space for China

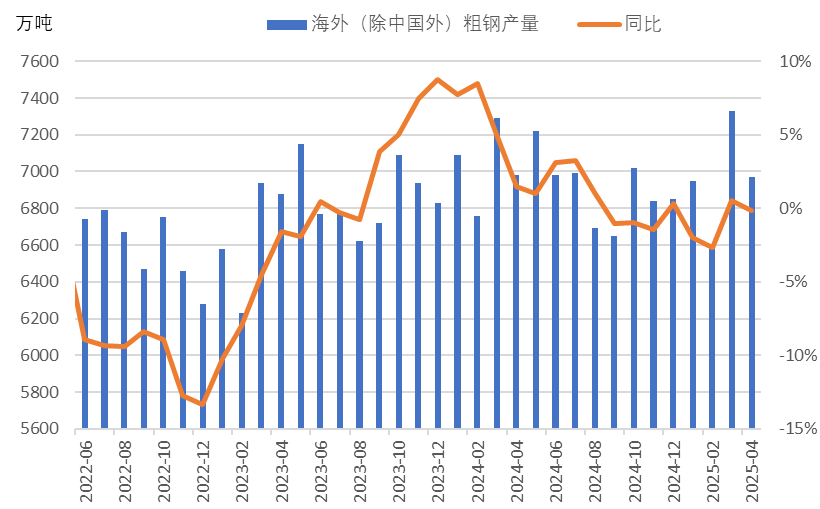

In April 2025, global crude steel production showed a year-on-year decrease. In April, the crude steel production of 69 countries included in the World Steel Association's statistics was 155.7 million tons, a year-on-year decrease of 0.3%. From the perspective of crude steel production outside China, the year-on-year growth has turned into a decline. Data monitored by Lange Steel Research Center shows that in April, the production in other regions of the world excluding China was 69.7 million tons, a year-on-year decrease of 0.1% (see Figure 3). The decrease in overseas supply has slightly released the external demand space for China's steel.

Figure 3: Monthly Crude Steel Production Outside China

3. Global Manufacturing PMI Remains in Contraction Range, External Demand Remains Weak

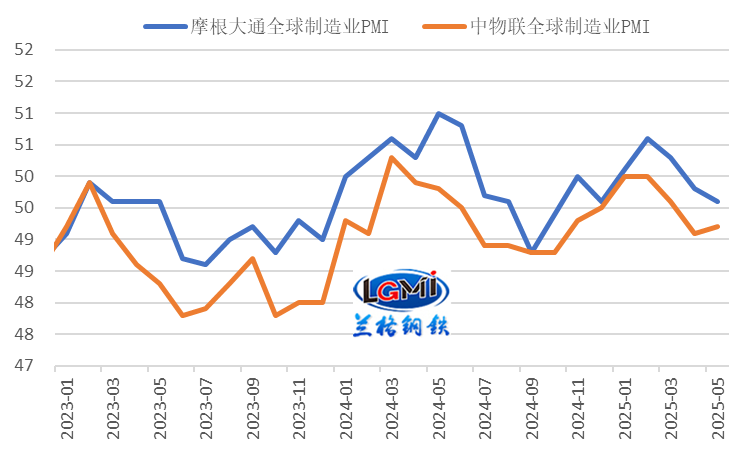

In May 2025, the global manufacturing PMI remained in the contraction range. According to the China Federation of Logistics and Purchasing, the global manufacturing PMI in May 2025 was 49.2% (see Figure 4), up 0.1 percentage points from the previous month. JPMorgan's global manufacturing PMI in May continued to fall in the contraction range, reaching 49.6%, down 0.2 percentage points from the previous month. The US additional tariffs still disrupt the global economy, increasing the uncertainty of global economic recovery, limiting the ability of enterprises in various countries to make long-term plans, and weakening the global economic recovery capacity in the short term. Based on the uncertainty caused by the US additional tariffs, the OECD's latest report lowered its forecast for world economic growth in 2025 from 3.1% to 2.9%. The UN predicts that global economic growth will slow to 2.4% in 2025, 0.4 percentage points lower than the January forecast.

Data released by the China Federation of Logistics and Purchasing and the Service Industry Survey Center of the National Bureau of Statistics show that in May, China's manufacturing new export order index was 47.5%, up 2.8 percentage points from the previous month. Although the export order index has rebounded, it is still in the contraction range, reflecting that the external environment remains complex and severe, and there is still uncertainty about the stabilization of foreign trade.

Figure 4: Global Manufacturing PMI (%)

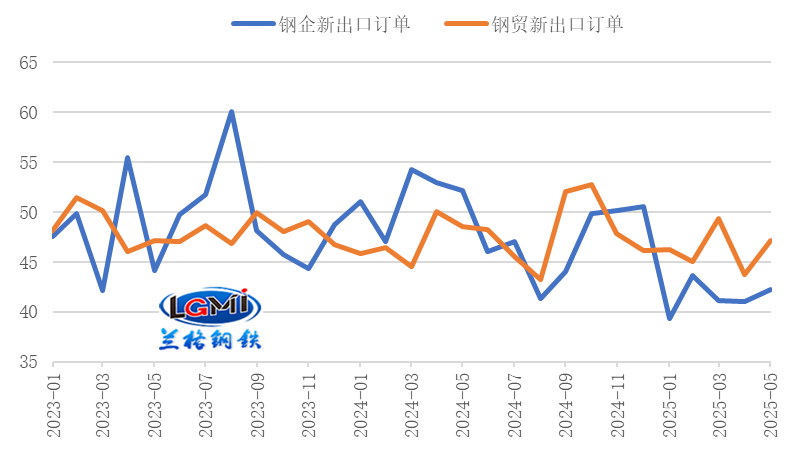

4. China's Steel Industry Export Order Index Rebounds Slightly in Contraction Range

From the perspective of steel export orders, the export order index of Chinese steel enterprises has rebounded slightly in the contraction range; the new export order index of steel enterprises surveyed by the China Federation of Logistics and Purchasing Steel Logistics Professional Committee in May 2025 was 42.2%, up 1.2 percentage points from the previous month (see Figure 5); the new export order index of steel circulation enterprises surveyed by the China Securities Depository and Clearing Corporation & Lange Steel Network was 47.1%, up 3.4 percentage points from the previous month. Although the steel industry's export order index has rebounded slightly in the contraction range, China's steel exports will still face pressure in the future.

Figure 5: Changes in the Steel Industry's New Export Orders (%)

5. Continued Trade Protection, Continued Pressure on China's Steel Exports

Since May, the trade frictions faced by China's steel industry have continued. On May 12, Canada launched anti-dumping and countervailing duty investigations into steel strip originating in or imported from China; on May 23, Pakistan launched an anti-circumvention investigation into cold-rolled steel sheets originating in or imported from China, examining whether the products involved have undergone minor changes (width exceeding 1250 mm) before being exported to Pakistan to circumvent anti-dumping duties; on June 3, Brazil launched an anti-dumping investigation into hot-rolled steel coils originating in China. According to data monitored by Lange Steel Research Center, as of June 9, 2025, other countries and regions have launched 18 trade remedy investigations against China's steel and steel products since the beginning of the year, doubling the number compared to the same period last year. China's steel industry still faces a severe foreign trade situation. In May, Malaysia made a positive final ruling on anti-dumping duties on tin-plated or coated iron or non-alloy steel flat-rolled products with a width greater than or equal to 600 mm originating in or imported from China, imposing anti-dumping duties based on CIF prices, with rates ranging from 4.48% to 20.42%; South Korea continued to impose anti-dumping duties for five years on stainless steel strip with a thickness of no more than 8 mm originating in China, with rates ranging from 23.69% to 25.82%; the EU made a positive final ruling on anti-dumping duties on tin-plated or coated iron or non-alloy steel flat-rolled products originating in China, with rates ranging from 13.1% to 62.3%.

On June 3, US President Trump announced that he would increase tariffs on imported steel, aluminum, and their derivatives from 25% to 50%. Currently, tariffs on some steel products directly exported to the US from China have reached 95%. Since China exported 890,000 tons of steel to the US in 2024, accounting for only 0.8% of total steel exports, the impact is relatively small, but it may have a greater inhibitory effect on re-export trade. Currently, China and the US have started the second round of trade talks in London, and the outcome of future talks remains to be seen.

In summary, China's steel export price advantage still exists. Although the steel industry's export order index has rebounded somewhat from the contraction range, the trend of trade protection continues, and the suppression of steel exports will gradually become apparent. Steel exports in June are expected to remain relatively high. Based on the month-on-month decline in the export base of steel in June 2024 (8.74 million tons), steel exports in June 2025 may still show growth. (Original article by Wang Guoqing, Lange Steel Research Center; please indicate the source if reproduced)

2025-06-09

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com