2025-07-07

Steel companies' profitability may improve under the policy background of "anti-involution"

From January to May 2025, driven by the implementation of China's steady growth and incremental policies, cost reductions, and export-boosting effects, the steel industry's profits continued to improve. Data from the National Bureau of Statistics show that from January to May 2025, the ferrous metal smelting and rolling processing industry achieved operating revenue of 3136.45 billion yuan, a year-on-year decrease of 7.0%; operating costs were 2985.77 billion yuan, a year-on-year decrease of 8.7%; total profit was 31.69 billion yuan; the same period last year was a loss of 12.72 billion yuan, turning from a loss to a profit year-on-year. In terms of a single month, in May, the ferrous metal smelting and rolling processing industry's profit was 14.77 billion yuan, setting a new high for monthly profits this year.

In June, under the influence of factors such as continuous disturbances from external geopolitical conflicts, the deepening of the domestic seasonal off-season effect, and the gradual restriction of the release of terminal demand, the domestic steel market showed a fluctuating downward trend. However, due to the larger decrease in costs, the profit margin of steel companies' short-term inventory raw material cycle has expanded. Looking ahead to July, the steel industry is entering the off-season for demand, and the demand for construction steel will further contract. How will the operating conditions of steel companies evolve? Lange Steel Research Center believes that there is still room for improvement in the steel industry's operations in July 2025.

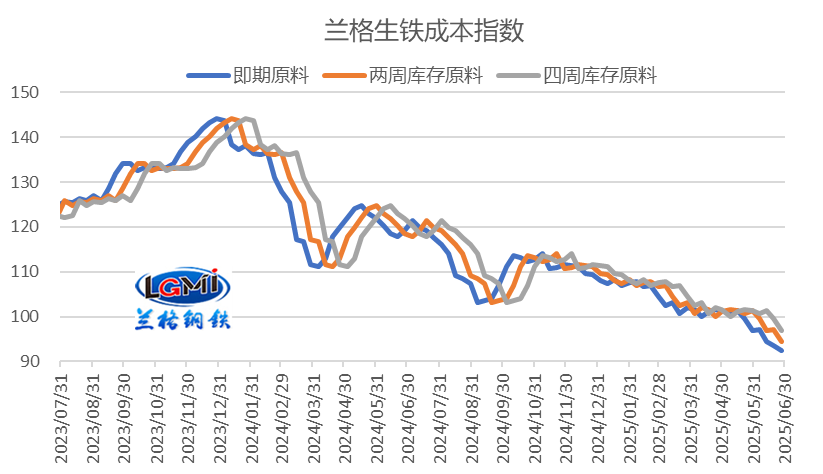

In June 2025, as raw material prices gradually declined, the average monthly cost also showed a downward trend. The average monthly cost calculated based on spot, two-week, and four-week inventory raw materials all fell. Lange Steel Research Center's monitoring data shows that in June, the spot raw material-based pig iron cost index was 94.3, down 5.3% year-on-year; the two-week inventory raw material-based pig iron cost index was 97.0, down 4.3% year-on-year; and the four-week inventory raw material-based pig iron cost index was 99.6, down 1.4% year-on-year. This shows that as raw material prices gradually fall, the shorter the inventory cycle, the greater the cost reduction.

Figure 1 Lange Pig Iron Cost Index Trend Chart

In terms of the average steel price, the Lange Steel Comprehensive Steel Price Index averaged 3443 yuan/ton in June, down 2.5% month-on-month; among them, the monthly average price of rebar was 3225 yuan, down 2.5% month-on-month; and the monthly average price of hot-rolled coils was 3284 yuan, down 2.4% month-on-month. From a cyclical perspective, due to changes in the raw material inventory cycle in June, there are some differences in cost reduction, so there is also a certain degree of differentiation in terms of profit per ton of steel.

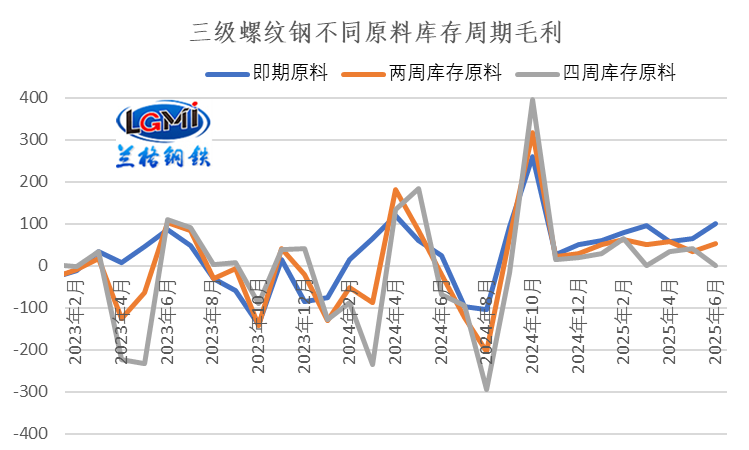

Looking at Grade III rebar, the average monthly gross profit of Grade III rebar calculated based on spot raw materials, two-week inventory raw materials, and four-week inventory raw materials in June was 102 yuan, 53 yuan, and 1 yuan, respectively, an increase of 36 yuan, 18 yuan, and a decrease of 40 yuan compared to the previous month. Under the condition of declining prices in the variety steel market, the cost reduction of the spot and two-week raw material inventory cycles was larger, leading to improved profitability, while the cost reduction of the four-week raw material inventory cycle was smaller, resulting in a decline in profitability (see Figure 2 for details).

Looking at hot-rolled coils, the calculated gross profit of hot-rolled coils in June also showed some differentiation. The profit calculated based on spot raw materials was 12 yuan, turning from a loss to a profit; the average monthly loss calculated based on two-week inventory raw materials was 37 yuan, a decrease of 11 yuan compared to the previous month; and the average monthly loss calculated based on four-week inventory raw materials was 89 yuan, an increase of 46 yuan compared to the previous month.

Figure 2 Changes in the Gross Profit Level of Grade III Rebar Calculated Based on Raw Materials with Different Inventory Cycles

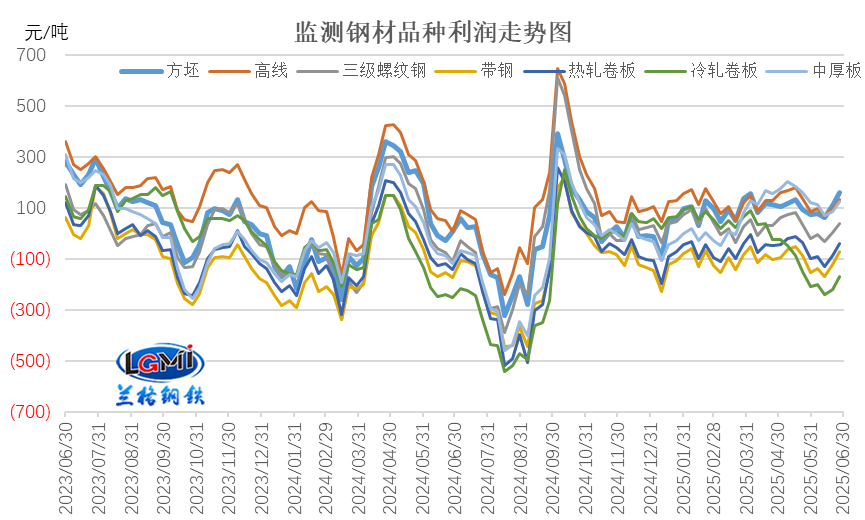

Looking at the gross profit performance of various products calculated based on four-week inventory raw materials, the gross profit of various products calculated based on four-week inventory raw materials in June showed a trend of first decreasing and then increasing, and the monthly profit of various products decreased; Lange Steel Research Center's monitoring data shows that among the seven major products monitored, the gross profit of cold-rolled coils decreased the most, by 86 yuan; the gross profit of billets decreased the least, by 2 yuan; and the gross profit of other products decreased by 36-69 yuan.

Figure 3 Gross Profit Level of Major Steel Products (Four-Week Inventory Raw Materials)

In general, under the combined influence of fluctuating and declining prices of variety steel and the gradual downward shift of production costs, the gross profit per ton of steel calculated based on spot, two-week, and four-week inventory raw materials in June showed some differentiation, with improved profitability for spot and two-week inventory raw materials and a decline in profitability for four-week inventory raw materials; it is expected that the steel company profit data officially released in June will still be relatively good.

The situation facing the steel industry in July remains complex and changeable. From the international environment, the global manufacturing PMI continues to decline, and the global economic recovery still faces resistance. Recently, the United States and various countries have gradually finalized tariffs, with the United States imposing a 20% tariff on exports to Vietnam; a 40% tariff on transshipment trade; and related tariffs will be determined later. Currently, according to reports, 70 countries have tariffs of 20-30%; about 100 countries may be subject to a benchmark equivalent tariff of 10%; and US-China tariffs are also expected to be finalized in July.

From the domestic environment, the endogenous driving force for expanding domestic demand in China still needs to be strengthened, and the foundation for the sustained and steady recovery of the economy still needs to be consolidated. China will adhere to the general work guideline of pursuing progress while ensuring stability, and fiscal and monetary policies are expected to further coordinate and strengthen, coordinating domestic economic work and international economic and trade struggles, unswervingly doing its own thing, placing greater emphasis on expanding domestic demand and strengthening the domestic cycle, focusing on stabilizing employment and the economy to promote high-quality development, and promoting sustained and healthy economic development.

From the supply side of the steel industry, the domestic steel market has entered the traditional off-season for demand, and many places have been significantly affected by rainfall, and the progress of outdoor construction has also been significantly restricted. At the same time, the manufacturing industry has also entered a "stable period" under high temperatures and heavy rains, so it is expected that domestic steel production in June will maintain a downward trend. According to Lange Steel Research Center's estimates, the daily crude steel output nationwide in June will remain at around 2.7 million tons. In July, under the situation of slowing demand, coupled with the reduction of iron and sintering production in Tangshan and the promotion of the industry's "anti-involution" policy, the release of crude steel production is expected to continue to decline.

From the demand side, in July, high temperatures and heavy rains will continue to increase, which will inhibit the construction of construction projects, and the demand for construction steel will further contract. The demand for steel in the manufacturing industry will maintain a certain resilience, but some industries will be under pressure.

From the cost side, the average price of raw materials fell in June, and the average monthly production cost of steel decreased significantly, further weakening the support of costs for steel prices.

In summary, the domestic steel market in July will still be affected by multiple factors. Since the end of June, due to domestic safety inspections and weakening imports, the stabilization and rebound of coking coal prices have shown some support at the bottom of costs, and coupled with Tangshan's production restrictions and the industry's "anti-involution" policy, market confidence has been boosted, and steel prices have shown a short-term rebound trend; however, as the off-season effect continues to deepen and insufficient demand continues to emerge, Lange Steel's big data AI-assisted decision-making system predicts that the domestic steel market in July will likely show a weak and fluctuating trend.

From the perspective of steel company profits, the domestic steel market in July 2025 will operate in a weak and fluctuating manner, with a phased rebound during the period, while costs are currently relatively low. Lange Steel Research Center expects that the operating profits of steel companies in July will have room for slight improvement. (Original article by Wang Guoqing, Lange Steel Research Center; please indicate the source if reprinted)

2025-12-08

2025-12-01

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com