2025-08-27

Steel companies' profits may once again face the risk of being "eroded"

Industry Data:

According to data from the National Bureau of Statistics, from January to July 2025, the ferrous metal smelting and rolling processing industry achieved operating revenue of 4,424.62 billion yuan, a year-on-year decrease of 6.6%; operating costs were 4,193.40 billion yuan, a year-on-year decrease of 8.4%; total profit was 64.36 billion yuan, a year-on-year increase of 5175.4%.

(Lange Steel Research Center, Ge Xin, 15810671409 (WeChat same number) Please indicate the source when reprinting)

Lange Commentary:

In July, driven by a strong industry atmosphere against internal competition, enhanced national expectations for expanding domestic demand, safe production limits on coking coal and coke, four rounds of price increases in the coke market, and strengthened cost support, the domestic steel market showed a fluctuating rebound. However, due to the continuous decline in raw material costs, the profit margin of the steel industry continued to expand. According to data released by the National Bureau of Statistics, from January to July 2025, the ferrous metal smelting and rolling processing industry made a profit of 64.36 billion yuan, a year-on-year increase of 5175.4%. Monthly data shows that the steel industry lost 1.55 billion yuan in January-February, made a profit of 9.06 billion yuan in March, 9.41 billion yuan in April, 14.77 billion yuan in May, 14.59 billion yuan in June, and 18.08 billion yuan in July, an increase of 3.49 billion yuan month-on-month.

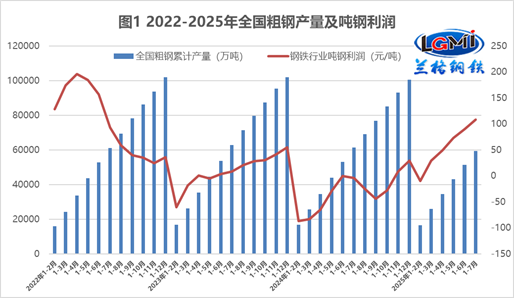

From the data on national crude steel output and profit per ton of steel, domestic steel producers were in a situation of "controlling production to expand profits" from January to July 2025, with a profit of 108 yuan per ton of steel, an increase of 112 yuan compared to the same period last year (see Figure 1). Operating costs continued to decline month-on-month from January to July but remained relatively high, with operating costs accounting for 94.8% of operating revenue, down 1.8 percentage points year-on-year (see Figure 2). Regarding steel company profit margins, profitability continued to strengthen from January to July, with a cost profit margin of 1.53%, up 1.59 percentage points year-on-year; sales profit margin was 1.45%, up 1.51 percentage points year-on-year (see Figure 3).

From January to July 2025, national pig iron and crude steel output declined year-on-year, while steel production increased year-on-year. According to data from the National Bureau of Statistics, from January to July, China's crude steel output was 594 million tons, down 3.1% year-on-year, with a cumulative daily output of 2.8041 million tons; pig iron output was 506 million tons, down 1.3% year-on-year, with a cumulative daily output of 2.386 million tons; steel production was 860 million tons, up 5.1% year-on-year, with a cumulative daily output of 4.0588 million tons. Among them, key statistical steel enterprises produced 490 million tons of crude steel, down 1.4% year-on-year, with a cumulative daily crude steel output of 2.3101 million tons; produced 437 million tons of pig iron, down 0.4% year-on-year, with a cumulative daily pig iron output of 2.0628 million tons; produced 493 million tons of steel, up 1.6% year-on-year, with a cumulative daily steel output of 2.3253 million tons. From the segmented production data of various steel categories, from January to July, the production of steel subcategories showed obvious differentiation; among construction steel varieties, rebar production declined relatively significantly year-on-year, while wire rod production slightly declined year-on-year; plate production increased significantly year-on-year; pipe and ferroalloy production also increased year-on-year (see Table 1).

Table 1: National Major Metallurgical Product Output from January to July 2025

From the data on major downstream product output, from January to July 2025, the adjustment of steel product demand structure continued, with more obvious year-on-year differentiation. However, steel demand in manufacturing remained better than in construction, with strong demand in machinery equipment manufacturing, engineering machinery, automobiles, ships, and home appliances manufacturing (see Table 2).

Table 2: National Steel Downstream Industrial Product Output from January to July 2025

The current international environment is complex and severe, with ongoing impacts from trade protectionism and unilateralism. Some domestic regions have experienced extreme weather such as high temperatures, heavy rain, and floods, causing short-term shocks to economic operations. Facing this complex situation, regions and departments have actively taken action, tackled difficulties, accelerated the implementation of more proactive macro policies, deeply promoted the construction of a unified domestic market, maintained continuous growth in production demand, overall stability in employment and prices, growth of new driving forces, and steady progress in economic operations. However, it should also be noted that there are many external unstable and uncertain factors, domestic market supply is strong while demand is weak, some structural contradictions remain apparent, and the foundation for economic recovery and improvement still needs to be consolidated. It is necessary to fully implement the decisions and deployments of the Party Central Committee, maintain policy continuity and stability, enhance flexibility and foresight, focus on stabilizing employment, enterprises, markets, and expectations, effectively promote the dual domestic and international circulation, and drive steady and healthy economic development.

Currently, the domestic steel market is gradually shifting from the off-season to the peak season. However, under the influence of multiple factors such as a severe and complex external environment, the resumption of China-US economic and trade negotiations, steady progress in the domestic economy, the end of regional production restrictions and time limits, and the gradual start of the traditional peak season, the domestic steel market in September may show a significant range-bound fluctuation. Moreover, since coke prices have already undergone seven rounds of increases, the main source of early steel mill profits is rapidly being "harvested." At the same time, under the overall supply surplus in the steel industry, structural adjustments in production and demand are continuously consolidating the product advantages of enterprises. (Lange Steel Research Center, Ge Xin, 15810671409 (WeChat same number) Please indicate the source when reprinting)

2025-12-08

2025-12-01

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com