2025-08-28

China Iron and Steel Association: Domestic steel prices stopped falling and rebounded in July

In July, under the continuous introduction of favorable national macro policies, increased cost support, and strengthened expectations for crude steel production control, the domestic steel market showed an upward trend.

Entering August, the domestic steel market gradually returned to fundamentals, with steel prices fluctuating slightly amid weak demand and continuous inventory accumulation.

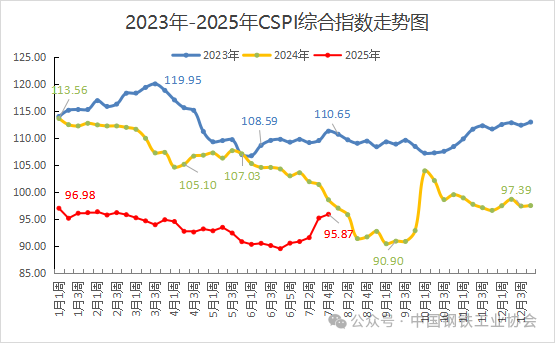

1. Domestic Comprehensive Steel Price Index Stops Falling and Rises

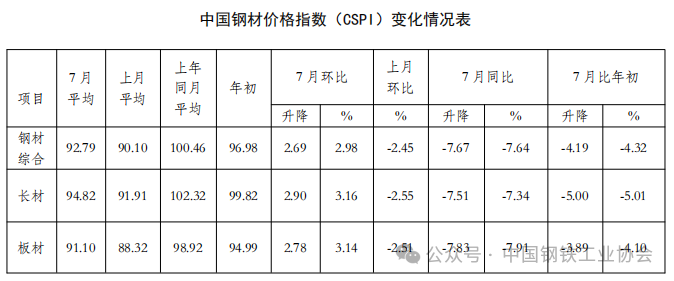

According to the Steel Association monitoring, in July 2025, the average CSPI value was 92.79 points, a month-on-month increase of 2.69 points, up 2.98%; year-on-year it decreased by 7.67 points, down 7.64%. Among them, the CSPI long product index average was 94.82 points, up 2.90 points month-on-month, an increase of 3.16%; year-on-year it decreased by 7.51 points, down 7.34%. The flat product index average was 91.10 points, up 2.78 points month-on-month, an increase of 3.14%; year-on-year it decreased by 7.83 points, down 7.91%.

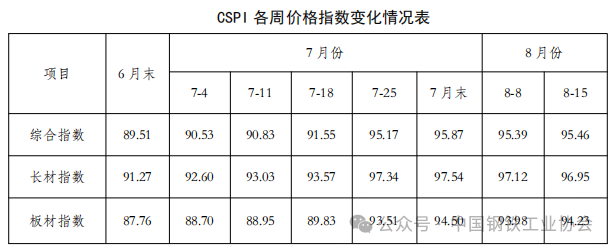

As of the end of July 2025, the China Steel Price Index (CSPI) was 95.87 points, up 6.36 points month-on-month, an increase of 7.11%; down 1.60 points compared to the end of last year, a decrease of 1.64%; year-on-year down 1.13 points, a decrease of 1.16%. (See the chart below)

From January to July, the average CSPI value was 93.58 points, down 13.28 points year-on-year, a decrease of 12.43%.

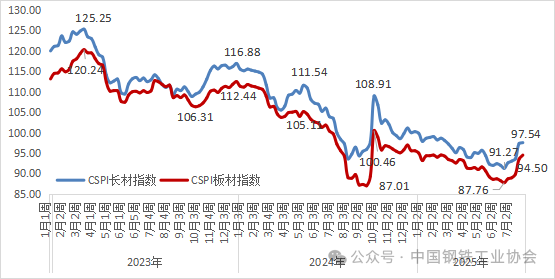

(1) Prices of long flat products have stopped falling and risen, with the month-on-month increase of long products smaller than that of flat products.

As of the end of July 2025, the CSPI long product index was 97.54 points, up 6.27 points month-on-month, an increase of 6.87%; the CSPI flat product index was 94.50 points, up 6.74 points month-on-month, an increase of 7.68%; compared with the same period last year, the CSPI long and flat product indices decreased by 0.81 points and 1.07 points respectively, down 0.82% and 1.12%.

From January to July, the average CSPI long product index was 95.57 points, down 13.69 points year-on-year, a decrease of 12.53%; the flat product index average was 91.89 points, down 13.52 points year-on-year, a decrease of 12.83%.

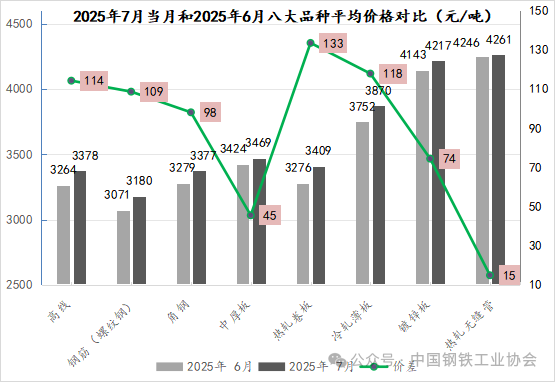

(2) Average prices of major steel products have risen comprehensively.

In July, among the eight major monitored steel products, the average prices of major steel products rose comprehensively. Among them, hot-rolled coil had a larger increase, with the average price rising by 133 yuan/ton, and the index rising by 4.07%; seamless pipes had a smaller increase, rising by 15 yuan/ton, with the index rising by 0.36%. (See the table below)

(3) Recently, the steel price index has been fluctuating at a high level.

Reviewing the steel market performance in the first half of the year: At the beginning of January, steel demand accelerated its decline, and the steel market was still in a supply-strong and demand-weak pattern, with prices fluctuating downward. In late January, as market sentiment improved, steel prices stopped falling and stabilized. After the Spring Festival, the domestic steel market experienced mild fluctuations downward due to increasing external shocks, slow downstream demand recovery, and production release exceeding demand. In March, the steel market continued to fluctuate sluggishly under the background of positive signals from the National Two Sessions, no fundamental improvement in the steel industry's supply-demand pattern month-on-month, and weak raw material prices, with the price center continuing to decline. In April, steel prices fluctuated downward. In May, the steel market transitioned from peak to off-season, with prices fluctuating downward. Entering June, under the influence of Trump's tariff policy and accumulating supply-demand contradictions, the market continued to consolidate and decline. By the end of June, the domestic comprehensive steel price index fell below 90.00 points, reaching 89.51 points, the lowest level since late November 2016. In July, the steel market showed an upward trend stimulated by the "anti-involution" policy, production restriction policies in some domestic regions, and resilient support from the raw material side. Entering August, the steel market gradually returned to fundamentals, fluctuating amid seasonal demand decline and continuous inventory accumulation. (See the table below)

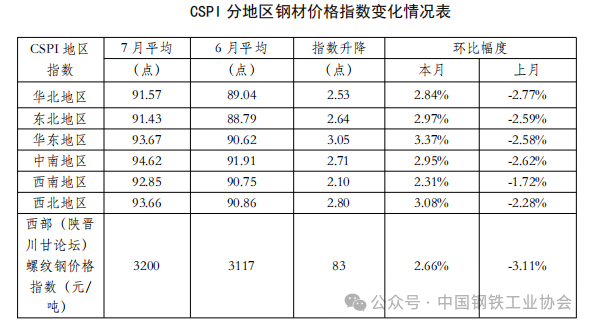

(4) The average steel price indices in various regions rose month-on-month.

By region, in July 2025, the average steel price indices of the six major regions nationwide showed a general upward trend. Among them, the East China region had a larger increase of 3.37%, while the Southwest region had a smaller increase of 2.31%.

In July, the average rebar price index in the western region (Shaanxi, Shanxi, Sichuan, Gansu Forum) was 3200 yuan/ton, up 83 yuan/ton month-on-month, an increase of 2.66%.

2. Analysis of Factors Affecting Domestic Steel Price Changes

(1) Growth rates of infrastructure investment, manufacturing investment, and real estate investment continue to decline.

From January to July 2025, national fixed asset investment (excluding rural households) was 28,822.9 billion yuan, a year-on-year increase of 1.6%, with the growth rate down 1.2 percentage points compared to January to June. Among them, infrastructure investment grew by 3.2% year-on-year, with the growth rate down 1.4 percentage points compared to January to June. Manufacturing investment grew by 6.2% year-on-year, with the growth rate down 1.3 percentage points compared to January to June 2025.

In July, under the background of intensifying implementation of more proactive macro policies, the national economy maintained steady and progressive development, and production demand continued to grow. In July, affected by the traditional production off-season in manufacturing, high temperatures, heavy rain, and flood disasters in some regions, the PMI dropped to 49.3%, with the manufacturing prosperity level slightly lower than last month. From both production and demand sides, expansion slowed, demand fell into contraction territory, with production and new order indices at 50.5% and 49.4%, down 0.5 and 0.8 percentage points respectively from last month. Manufacturing production activities continued to expand, but market demand slowed. The new export order index was 47.1%, down 0.6 percentage points from last month, continuing to operate in contraction territory, indicating some pressure on manufacturing exports. From January to July, industrial added value above designated size grew 6.3% year-on-year, with the growth rate down 0.1 percentage points compared to January to June.

From the perspective of the automobile manufacturing industry, according to the China Association of Automobile Manufacturers, from January to July, automobile production and sales reached 18.235 million and 18.269 million units respectively, up 12.7% and 12% year-on-year, with production and sales growth rates expanding by 0.2 and 0.6 percentage points compared to January to June. From the real estate industry perspective, from January to July, real estate development investment declined 12.0% year-on-year, with the decline expanding by 0.8 percentage points compared to January to June; new housing starts decreased by 19.4%, with the decline narrowing by 0.6 percentage points compared to January to June; the decline in new housing starts continues to narrow. The sales area of newly built commercial housing fell 4.0% year-on-year, with the decline expanding by 0.5 percentage points compared to January to June. In July, the National Real Estate Prosperity Index was 93.34, declining for four consecutive months, indicating the real estate industry remains weak.

Overall, from January to July 2025, all real estate indicators continued to decline, with the year-on-year decline in real estate development investment continuing to expand, and the National Real Estate Prosperity Index declining for four consecutive months, showing overall weakness and lack of confidence in the real estate market. Growth rates of infrastructure and manufacturing investment continued to decline, and current key indicators related to downstream steel-using industries in the steel sector continue to operate weakly.

(2) The apparent consumption decline of crude steel in the first 7 months is greater than the production decline.

According to the latest data released by the National Bureau of Statistics, from January to July, the national crude steel production was 594.47 million tons, a year-on-year decrease of 3.1%; in July, the daily crude steel production was 2.569 million tons, a month-on-month decrease of 7.4%. From January to July, China's pig iron production was 505.83 million tons, a year-on-year decrease of 1.3%; in July, the daily pig iron production was 2.284 million tons, a month-on-month decrease of 4.7%. From January to July, steel production was 860.47 million tons, a year-on-year increase of 5.1%; in July, the daily steel production was 3.966 million tons, a month-on-month decrease of 6.9%. In terms of imports and exports, from January to July, steel exports increased in volume but decreased in price year-on-year, while imports decreased in volume but increased in price year-on-year. The cumulative steel exports from January to July were 67.983 million tons, an increase of 6.96 million tons or 11.4% year-on-year, with an average price of 699.7 USD/ton, down 80.9 USD/ton or 10.4%; cumulative steel imports were 3.476 million tons, a decrease of 646,000 tons or 15.7%, with an average price of 1701.9 USD/ton, up 37.0 USD/ton or 2.2% year-on-year.

Based on this calculation, the national apparent consumption of crude steel (excluding steel billets) from January to July was 519.36 million tons, a year-on-year decrease of 6%. The decline in crude steel production in the first 7 months was significantly less than the decline in apparent consumption, indicating a supply-strong and demand-weak pattern in the domestic steel market in July.

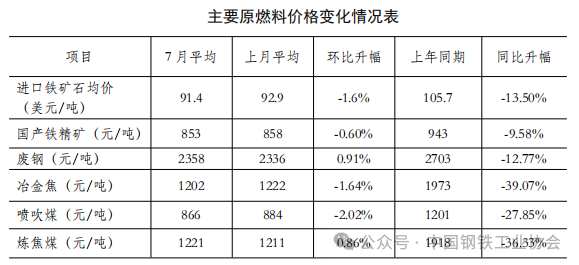

(3) The average prices of major raw materials and fuels showed mixed changes.

Regarding raw materials and fuels, compared with June, the average prices of major raw material varieties showed mixed changes. The average prices of imported iron ore, domestic iron concentrate, metallurgical coke, and pulverized coal injection decreased month-on-month, among which pulverized coal injection dropped significantly by 2.02%, while domestic ore decreased slightly by 0.60%. The average prices of scrap steel and coking coal both rose slightly, with increases not exceeding 1%. (See the table below)

3. International market steel prices continue to decline.

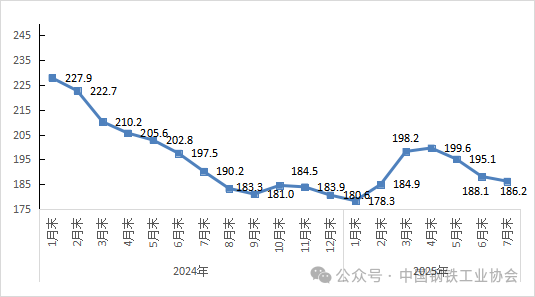

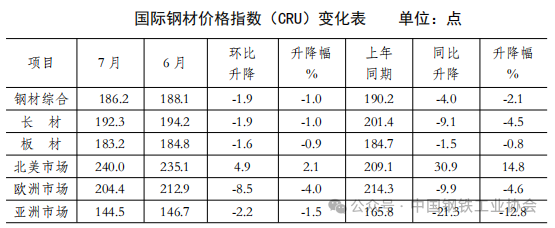

In July 2025, the CRU International Steel Price Index was 186.2 points, down 1.9 points month-on-month, a decrease of 1.0%; down 4.0 points year-on-year, a decrease of 2.1%. (See the chart below)

CRU International Steel Price Index Trend Chart.

From January to July 2025, the average CRU International Steel Price Index was 190.1 points, down 18.1 points year-on-year, a decrease of 8.7%. Among them, the average CRU long products index was 195.4 points, down 15.4 points year-on-year, a decrease of 7.3%; the average CRU flat products index was 187.4 points, down 19.4 points year-on-year, a decrease of 9.4%.

(1) Prices of long and flat products continued to decline.

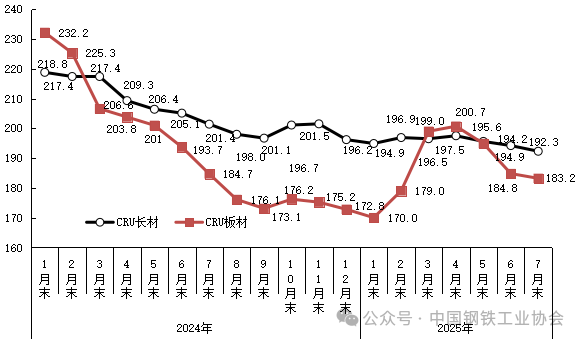

In July 2025, the CRU long products index was 192.3 points, down 1.9 points month-on-month, a decrease of 1.0%; the CRU flat products index was 183.2 points, down 1.6 points month-on-month, a decrease of 0.9%; compared with the same period last year, the CRU long products index decreased by 9.1 points, a decrease of 4.5%; the CRU flat products index decreased by 1.5 points, a decrease of 0.8%. (See the chart below)

CRU Long and Flat Products Price Index Trend Chart.

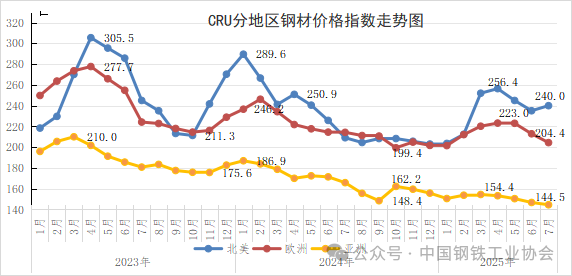

(2) North American steel price index turned from decline to rise, while Asia and Europe continued to decline.

1. North American market.

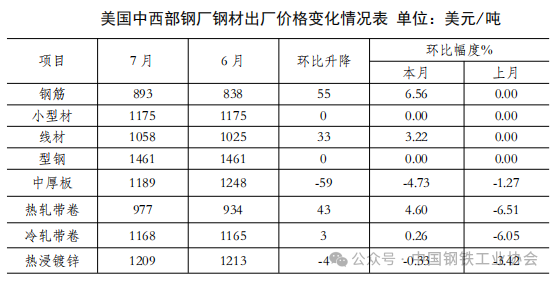

In July 2025, the CRU North American Steel Price Index was 240.0 points, up 4.9 points month-on-month, an increase of 2.1%; the US manufacturing PMI was 48%, down 1 percentage point month-on-month. This month, steel product trends in US Midwest steel mills diverged: rebar, wire rod, and hot-rolled coil prices rose significantly, with rebar increasing by 6.56%, wire rod by 3.22%, cold-rolled coil remained stable with slight increases, small sections and structural steel prices remained stable, hot-dip galvanized steel slightly decreased, and medium-thick plates dropped significantly by 4.73%. (See the table below)

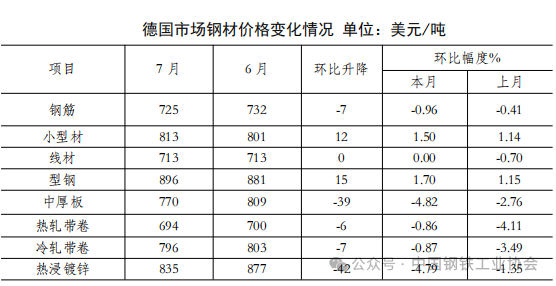

2. European market.

In July, the CRU European Steel Price Index was 204.4 points, down 8.5 points month-on-month, a decrease of 4.0%; in July 2025, the Eurozone manufacturing PMI final value was 49.8, continuing to rise from the previous month and close to the 50-point threshold between expansion and contraction. The Eurozone manufacturing sector continued a slow recovery trend with a slight improvement from the previous month. Major member countries all showed increases: Germany, France, Italy, and Spain manufacturing PMI indices rose to 49.1%, 48.2%, 49.8%, and 51.9%, respectively, up 0.1, 0.1, 1.4, and 0.5 percentage points. This month, the German market showed divergent price trends for major steel products: rebar, hot-rolled coil, and cold-rolled coil slightly decreased; medium-thick plates and hot-dip galvanized steel dropped significantly, both close to 5%; small sections and structural steel slightly increased; wire rod remained stable. (See the table below)

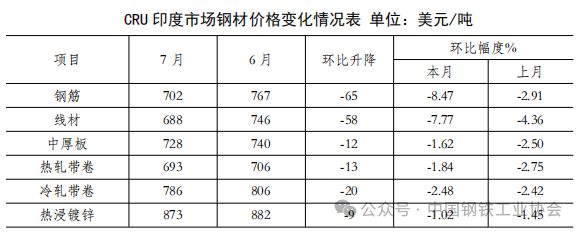

3. Asian market.

In July 2025, the CRU Asian Steel Price Index was 144.5 points, down 2.2 points from the previous month, a decrease of 1.5%; Japan's manufacturing PMI was 48.9%, down 1.2 percentage points month-on-month; South Korea's manufacturing PMI was 48%, down 0.7 percentage points month-on-month; India's manufacturing PMI was 59.1%, up 0.7 percentage points month-on-month. In July 2025, China's manufacturing PMI was 49.3%, down 0.4 percentage points from June. In the Indian market this month, prices of major steel products all declined, with rebar dropping significantly by 8.47%, and hot-dip galvanized steel, medium-thick plates, and hot-rolled coil prices all slightly decreasing. (See the table below)

4. Analysis of future steel price trends.

From the macroeconomic perspective, the current international situation is increasingly complex, and the global economy in 2025 still faces significant vulnerabilities. According to data released by the China Federation of Logistics & Purchasing, the global manufacturing PMI in July 2025 was 49.3%, down 0.2 percentage points from the previous month, ending a two-month consecutive month-on-month increase. The global manufacturing purchasing managers index has been in contraction territory for five consecutive months, indicating continued weakness in global manufacturing. On July 29, the International Monetary Fund (IMF) released the latest "World Economic Outlook," forecasting global economic growth rates of 3.0% and 3.1% for this year and next year, respectively, revised upward by 0.2 and 0.1 percentage points from the April forecast. The upward revision is mainly due to: the front-loading effect of imports and exports under tariff expectations being stronger than expected, the average effective tariff rate in the US being lower than the level announced in April, and some major economies implementing fiscal expansion. Although the global economic growth forecast has been slightly raised, the report indicates that the global economic recovery still faces significant downward pressures: the rebound in effective tariff rates may hinder economic growth, rising uncertainty may have more severe negative impacts on economic activity, geopolitical tensions may disrupt global supply chains and push up commodity prices, etc.

Domestically, on April 25, the Political Bureau of the CPC Central Committee held a meeting and believed that the economy has shown an improving trend this year, but the foundation for sustained recovery and improvement still needs to be consolidated. External shocks have increased, requiring the implementation of more proactive and effective macro policies, full use of fiscal and monetary policies, acceleration of bond issuance, timely reserve requirement ratio and interest rate cuts, and the creation of new policy tools. On May 7, the State Council Information Office held a press conference to introduce the "Package of Financial Policies to Support Market Stability and Expectation Stabilization." At the meeting, the central bank released 3 categories of 10 measures, including interest rate cuts, reserve requirement ratio cuts, and reductions in housing provident fund interest rates, which will effectively alleviate the financing pressure on steel enterprises and downstream steel-using industries and improve market liquidity. On July 30, the Political Bureau of the CPC Central Committee held a meeting emphasizing that to do a good job in economic work in the second half of the year, policy continuity and stability must be maintained, with enhanced flexibility and foresight. The construction of a unified national market will be advanced in depth, market competition order continuously optimized, disorderly competition among enterprises governed according to law and regulations, and capacity governance in key industries promoted. The meeting required the implementation of more proactive fiscal policies and moderately loose monetary policies in detail, effectively releasing domestic demand potential. On August 1, the central bank held a work meeting for the second half of 2025, stating that a moderately loose monetary policy should be implemented in the second half of the year, the reserve requirement ratio lowered, various monetary policy tools flexibly used, and liquidity kept ample. From this, it can be seen that loosening monetary policy, expanding fiscal policy, countering internal competition, and expanding domestic demand will be the main focuses of China's economic policy in the second half of the year, conducive to stable economic growth.

Under the background of declining demand and ample supply of raw materials, steel prices are mainly affected by the market supply side. Since the Spring Festival, demand has recovered slowly, and supply remains the key factor determining the future trend of steel prices. On March 13, the National Development and Reform Commission proposed to continue controlling crude steel output in 2025 and promote the reduction and restructuring of the steel industry. On July 1, the Central Financial and Economic Affairs Commission held its sixth meeting, emphasizing the need to govern enterprises' low-price disorderly competition according to law and regulations, promote the orderly exit of backward capacity, and release a new national-level "anti-internal competition" policy signal. On July 18, the State Council Information Office held a press conference where Xie Shaofeng, Chief Engineer of the Ministry of Industry and Information Technology, stated that the next step will be to implement a new round of growth stabilization plans for ten key industries including steel, non-ferrous metals, petrochemicals, and building materials, promoting structural adjustment, supply optimization, and elimination of backward capacity in key industries. In addition, the Central Political Bureau meeting at the end of July listed "governing disorderly competition among enterprises according to law and regulations" and "promoting capacity governance in key industries" as key tasks, continuing the tone of strengthening "anti-internal competition" since 2025. It is expected that the crude steel output control policy will be concentrated and implemented in the second half of the year, and the pattern of strong supply and weak demand may improve.

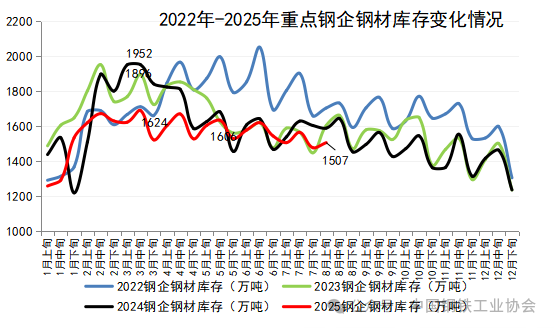

From the perspective of output, the daily crude steel production of key statistical steel enterprises rebounded in early August. In early August 2025, key statistical steel enterprises produced a total of 20.74 million tons of crude steel, with an average daily output of 2.074 million tons, a 4.7% increase in daily output compared to the previous period.

From the perspective of enterprise inventory, enterprise inventory is at a relatively low level compared to the same period in recent years. In early August 2025, key statistical steel enterprises had a steel inventory of 15.07 million tons, an increase of 290,000 tons compared to the previous ten-day period, a 2.0% increase, an increase of 2.7 million tons compared to the beginning of the year, a 21.8% increase, basically flat compared to the same ten-day period last month, and a decrease of 830,000 tons compared to the same ten-day period last year, a 5.2% decrease.

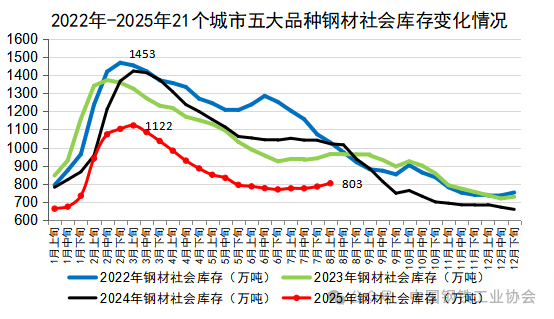

From the perspective of social inventory, since mid-July, social inventory has shown a continuous accumulation trend. By early August, the social inventory of five major steel varieties in 21 cities reached 8.03 million tons, an increase of 180,000 tons compared to the previous period, a rise of 2.3%, an increase of 1.44 million tons compared to the beginning of the year, a rise of 21.9%, and a decrease of 2.18 million tons compared to the same period last year, a decline of 21.4%.

Main issues to watch in the future:

Steel exports face significant pressure in the second half of 2025. Under the "export rush" effect, China's steel exports from January to July increased by 11.4% year-on-year, but this trend may not be sustainable. On one hand, in 2024, there were as many as 33 trade remedy cases against Chinese steel export products, with the process from filing to final ruling generally taking 10 to 18 months. The second half of 2025 will see a concentration of arbitration periods, greatly increasing direct export pressure on Chinese steel. In the first half of 2025, there were already 17 trade remedy investigation cases. On the other hand, the tariff war initiated by the Trump administration in the United States has also brought significant pressure to global steel exports. On May 30, the White House announced that the U.S. steel import tariff would increase from 25% to 50%. On June 12, the U.S. Department of Commerce announced that starting June 23, tariffs of 50% would be imposed on various steel household appliances, indirectly affecting China's steel exports. From July 28 to 29, a new round of China-U.S. economic and trade talks was held. According to the consensus, both sides will continue to promote the 90-day extension of the suspended U.S. reciprocal tariff of 24% and China's countermeasures. Although the 90-day extension avoids the immediate resumption of tariffs, providing a buffer period for export enterprises and reducing the risk of order loss in the short term, the uncertainty of tariff renewal after 90 days remains, and enterprises still face policy uncertainty risks and need to continuously cope with supply chain adjustment pressures. Meanwhile, starting in August, the U.S. will impose different rates of reciprocal tariffs on other countries worldwide, which is expected to have some impact on China's steel exports. Overall, the international trade environment for China's steel industry in the latter half of 2025 will be more complex, and high-level steel exports may not be sustainable. Steel enterprises should closely monitor changes in international market demand, the impact of global trade protectionism trends on exports, and timely adjust export strategies.

Steel enterprises need to pay attention to the price governance mechanism and regulate their own steel product market pricing. On April 2, 2025, the General Office of the CPC Central Committee and the General Office of the State Council issued the "Opinions on Improving the Price Governance Mechanism," specifically mentioning "improving the social price supervision system and establishing a price supervisor system by industry associations." On July 24, the National Development and Reform Commission and the State Administration for Market Regulation solicited public opinions on the "Amendment Draft of the Price Law of the People's Republic of China (Draft for Comments)," proposing to improve the identification standards for low-price dumping, regulate market price order, govern "internal competition" behavior, and improve the identification standards for unfair pricing behaviors such as price collusion, price gouging, and price discrimination. For the steel industry, the supply side will achieve "quality improvement and quantity reduction" through eliminating inefficient capacity and promoting technological innovation, while rectifying illegal acts such as selling below cost. After policy implementation, low-price vicious competition will decrease, and steel prices will more truly reflect supply-demand relationships and costs. Steel enterprises need to respond to the policy call, take compliant pricing as the baseline, turn policy constraints into opportunities for industry integration and value chain upgrading, and closely follow feedback on the solicitation and subsequent detailed rules implementation.

Steel enterprises should reasonably arrange production rhythm and continue to maintain self-discipline in production control. On one hand, although supply declined in July, with nationwide high temperatures and heavy rains reaching peak periods, the operating rates of major construction machinery products in July continued to decline year-on-year and month-on-month, reflecting insufficient activity in infrastructure and real estate construction, further pressuring the demand side. Social steel inventory gradually accumulated, and the industry showed a clear feature of strong supply and weak demand. Entering August, due to the current industry profit margin still being acceptable, steel mills' willingness to release capacity remains resilient, and short-term production decline space is limited. However, demand continues to decline, inventory continues to accumulate, and fundamental pressure gradually increases. On the other hand, crude steel output control policies will be concentrated and implemented later. Steel enterprises need to strictly implement national crude steel output control policies, self-discipline in production control, and timely and reasonably arrange production plans. (China Iron and Steel Association)

2025-12-08

2025-12-01

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com