2025-10-15

Steel companies still face downward pressure on profitability in October.

In August 2025, the steel industry continued to see improving business performance. According to data from the National Bureau of Statistics, from January to August 2025, the ferrous metal smelting and rolling industries achieved operating revenue of 5,079.98 billion yuan, a year-on-year decrease of 5.3%. Meanwhile, operating costs fell by 7.5% to 4,804.69 billion yuan, while total profits turned positive, rising to 83.7 billion yuan—a significant turnaround from previous losses. Looking specifically at August, the ferrous metal smelting and rolling sector recorded a profit of 19.34 billion yuan, an increase of 1.26 billion yuan compared to the previous month. Notably, this marked the first time in the year that monthly profits exceeded 19 billion yuan, setting a new high for the period.

In September, amid a complex and challenging external environment, coordinated macroeconomic policies, gradually strengthening supply releases, limited recovery in demand during the traditional peak season, divergent market performance, resilient cost support, and escalating trade tensions, China's domestic steel market experienced volatile yet weakening price trends, leading to a narrowing profit margin for steelmakers. Looking ahead to October, as the steel industry remains in its peak demand period, how will steel companies' business conditions evolve? According to the Lange Steel Research Center, the iron and steel sector's profit margins are likely to continue contracting in October 2025.

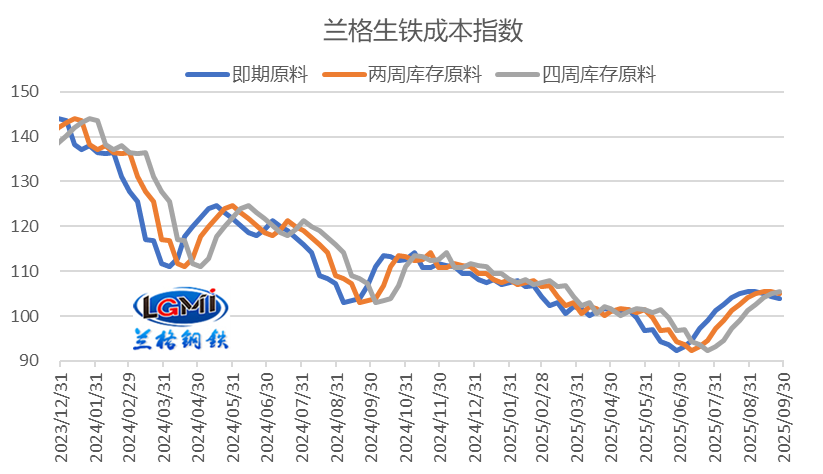

In September 2025, as raw material prices gradually climbed, the average monthly costs calculated for spot, two-week, and four-week inventory stocks of raw materials continued to rise. According to monitoring data from the Lange Steel Research Center, the spot raw material-based pig iron cost index in September stood at 104.7, up 1.0% from the same period last month; the two-week inventory-based pig iron cost index reached 105.3, an increase of 4.4% compared to the previous month; and the four-week inventory-based index surged to 104.3, a sharp 7.5% rise from the prior month. This trend highlights that as raw material prices stabilize after their initial surge, the longer the inventory cycle, the greater the corresponding increase in costs.

Figure 1: Trend Chart of the Langel Iron Cost Index

Looking at the average steel prices, Lange Steel's comprehensive steel price index averaged 3,560 yuan per ton in September, down 1.6% from the previous month. Among these, the average monthly price of threaded steel was 3,300 yuan, a 2.3% decline from the prior month, while the average monthly price of hot-rolled coil sheets fell by 1.5% to 3,478 yuan per ton. From a cyclical perspective, September saw some increases in costs due to changes in raw material inventory cycles, yet steel prices continued to drop. As a result, profitability per ton of steel experienced a noticeable decline.

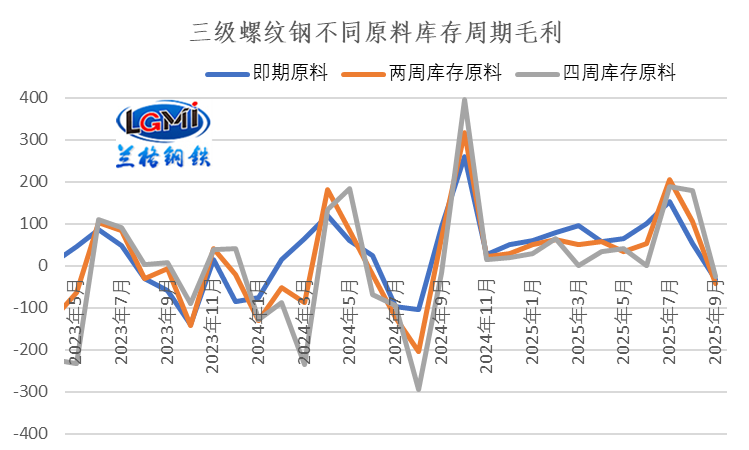

Looking at Grade-III rebar, the average monthly gross profits for spot raw materials, two-week inventory materials, and four-week inventory materials in September were -¥33, -¥42, and -¥26 per ton, respectively—down by ¥86, ¥147, and ¥205 compared to the previous month. Profitability has turned negative across all three raw material inventory cycles. Notably, the cost increases were more pronounced during the two- and four-week inventory periods, leading to a sharper decline in profitability (see Figure 2 for details).

Looking at hot-rolled coil, the calculated gross profit for September also showed a slight weakening. Specifically, the immediate, two-week, and four-week inventory-based gross profits were -7 yuan, -121 yuan, and -1 yuan, respectively—down 59 yuan, 121 yuan, and 179 yuan from the previous month. Notably, the longer the inventory cycle, the greater the decline in gross profit.

Figure 2: Changes in Gross Profit Levels for Raw Materials Calculated Across Different Inventory Cycles of Grade-3 Rebar

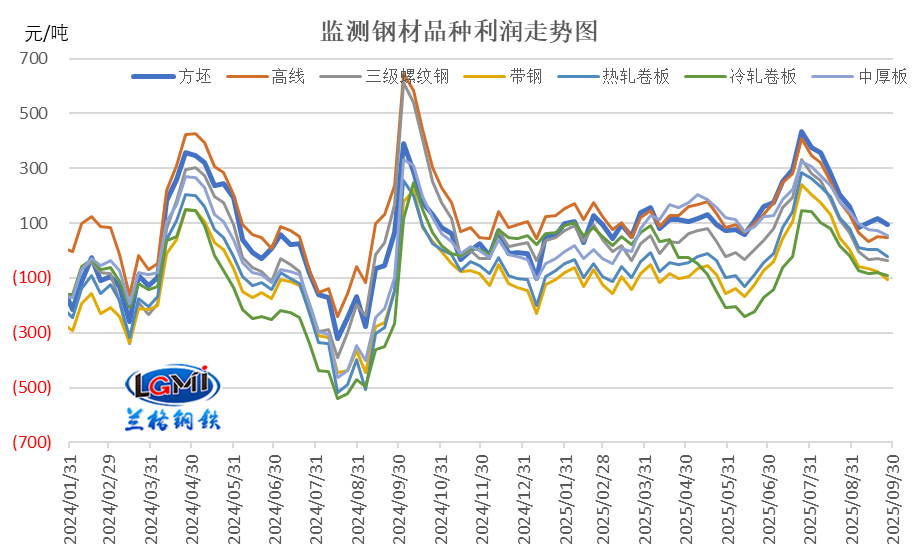

Analyzing the gross profit performance of various steel products based on four-week inventory data, September showed a trend of initially sharp declines followed by minor fluctuations. As a result, the average monthly profitability for all monitored products decreased. According to data from the Lange Steel Research Center, among the seven major steel varieties tracked, the monthly gross profit for each declined by between 147 and 205 yuan. Notably, only billets, high wire, and medium-to-thick plates managed to maintain some level of profitability, with profit margins ranging from 49 to 99 yuan. Meanwhile, all other product categories remained in the red, with losses varying from 1 to 83 yuan per ton.

Figure 3: Gross Profit Levels for Key Steel Products (Raw Materials in Inventory Around the Perimeter)

Overall, under the combined impact of high-grade material prices retreating from their peaks and gradually rising production costs, the estimated gross profit per ton of steel for spot, two-week, and four-week inventory raw materials all deteriorated in September. Steel companies' profit figures, as reported in September statistics, are expected to have weakened compared to the previous month.

In October, the steel industry continues to face a complex and dynamic situation. From the global perspective, although the global manufacturing PMI has slightly declined, the fluctuations remain relatively mild, indicating that the global economic recovery remains fairly steady. In fact, the pace of global economic recovery in the third quarter improved compared to the second quarter. Meanwhile, China's manufacturing sector saw a modest improvement in external demand, as evidenced by the continued rebound of the country's manufacturing export order index, which had been stuck in contraction territory. This positive trend was driven by several key factors: the ongoing strengthening of advantages in China's "new three" industries, the steady performance of traditional export-oriented equipment sectors, and the continued advancement of strategies aimed at diversifying export markets—collectively helping to curb the downward momentum in manufacturing export demand.

From the perspective of the domestic environment, China's economy continues to maintain a steady yet progressive development trend. Moving forward, we will continue to implement and refine various macroeconomic policies, with a strong focus on stabilizing employment, supporting businesses, safeguarding markets, and managing expectations. At the same time, we will deepen reform, expand opening-up, and foster innovation to drive the economy toward stable, healthy, and sustainable growth.

From the supply side of the steel industry, the domestic steel market is currently at a critical stage where peak-season demand is finally being released. However, downstream demand—as reflected in nationwide economic data—is not looking optimistic. Coupled with the impact of policies aimed at curbing "internal involution" and controlling production, crude steel output in the second half of the year has consistently remained low. As a result, domestic steel production in September and October is expected to stay relatively subdued.

From the demand side, in October—traditionally the peak season known as "Silver October"—construction project activities are expected to recover somewhat, leading to a rebound in demand for construction steel. Meanwhile, steel demand from the manufacturing sector is likely to remain steady.

From the cost perspective, the average price of raw materials continued to rise in September, leading to a slight increase in the monthly average production cost of steel. As a result, cost support for steel prices has strengthened somewhat. Since October, with the first round of coking coal price hikes taking effect, iron ore prices have remained firm, pushing steel production costs higher once again.

Overall, the domestic steel market in October continued to be influenced by multiple factors. Uncertainty surrounding China-U.S. tariff negotiations has intensified, while downstream demand has failed to pick up as strongly as expected. Meanwhile, social steel inventories remain under significant pressure. Although supply levels have stayed relatively low and cost support has strengthened somewhat, the evolving balance between supply and demand still requires close monitoring. According to Lang Steel’s big data AI-assisted decision-making system, the domestic steel market is projected to experience weak, volatile price movements in October 2025, with average prices likely continuing their downward trend compared to the previous month.

From the perspective of steel companies' profitability, the steel market in October 2025 is expected to remain weak and volatile, with average steel prices likely to continue declining from the previous month. Amidst persistently high and resilient raw material costs, Lange Steel Research Center forecasts that steel firms will still face downward pressure on their operating profits in October. (Original article by Wang Guoqing, Lange Steel Research Center; please attribute the source when reprinting.)

2025-12-08

2025-12-01

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com