2025-10-16

Credit coordination of supply and demand will help the steel market navigate the "seasonal transition."

Macroeconomic Data:

According to statistics from the People's Bank of China, as of the end of September 2025, the broad money supply (M2) stood at 335.38 trillion yuan, representing an 8.4% year-on-year increase. Meanwhile, the narrow money supply (M1) totaled 113.15 trillion yuan, up 7.2% compared to the same period last year. In the first three quarters, RMB loans increased by 14.75 trillion yuan; meanwhile, the cumulative incremental size of social financing reached 30.09 trillion yuan, an increase of 4.42 trillion yuan compared to the same period last year.

(Lange Steel Research Center, Ge Xin, 15810671409 [WeChat account also available]; please credit the source when reprinting)

Lange's commentary:

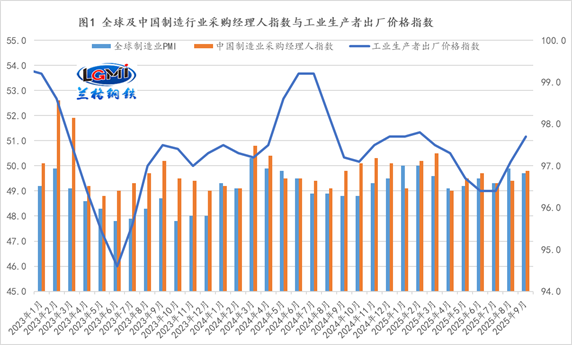

In September 2025, influenced by factors such as the deepening construction of the nationwide unified market, improvements in supply-demand structures, upgrades in industrial sectors, and the release of consumption potential, China's PPI remained unchanged month-on-month for the second consecutive month. Meanwhile, the year-on-year decline continued at 2.3%, though this drop narrowed by 0.6 percentage points compared to the previous month (see Figure 1 for details). Currently, the cumulative effects of multiple domestic policies aimed at stabilizing growth are becoming more evident. However, it is also crucial to significantly strengthen macroeconomic policy measures designed to counter-cyclically adjust the economy, thereby boosting the sustained recovery of demand for steel used in manufacturing.

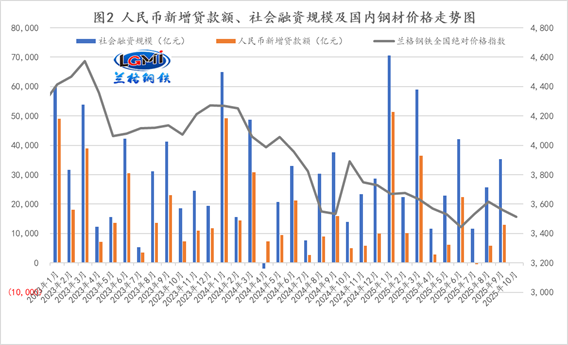

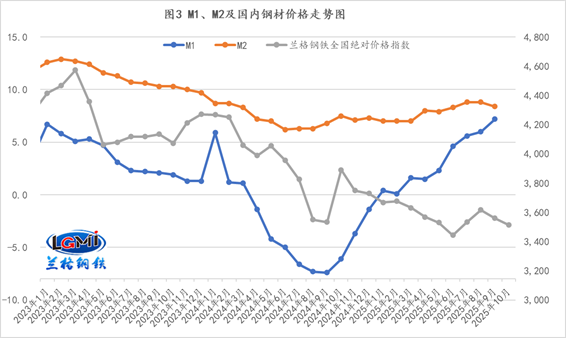

Looking at the financial data from January to September, credit and social financing showed a diverging trend compared to the same period last year: while new RMB loans increased at a slower pace year-on-year, the total increment in social financing saw a significant year-on-year rise (see Figure 2 for details). Meanwhile, narrow money (M1) posted positive year-on-year growth for the ninth consecutive month, with its growth rate continuing to accelerate, whereas broad money (M2) experienced a slight deceleration in its year-on-year growth rate (see Figure 3 for details).

From the lending perspective, corporate loans increased by 13.44 trillion yuan from January to September, including a rise of 4.53 trillion yuan in short-term loans and 8.29 trillion yuan in medium- and long-term loans, along with an additional 475.2 billion yuan in bill financing. This indicates that businesses continue to show growing confidence in both short-term and medium-to-long-term investments, though their willingness to manage short-term risks has slightly strengthened. Meanwhile, household loans totaled 1.1 trillion yuan from January to August, with short-term loans declining by 230.4 billion yuan and medium- and long-term loans rising by 1.33 trillion yuan—reflecting that consumer demand for borrowing remains relatively subdued.

From the perspective of social financing, from January to September, the incremental scale of social financing reached 30.09 trillion yuan, an increase of 4.42 trillion yuan compared to the same period last year. Among them, RMB loans extended to the real economy rose by 14.54 trillion yuan, although this was 851.2 billion yuan less than the previous year's growth. Meanwhile, net corporate bond financing stood at 1.57 trillion yuan, down 15.1 billion yuan year-on-year; in contrast, net government bond financing hit 11.46 trillion yuan, up 4.28 trillion yuan compared to the same period last year. This suggests that while government bond financing remains relatively robust, corporate financing demand is showing signs of recovery.

Since the beginning of this year, in the face of a complex and challenging external environment and various economic difficulties, regions and departments have earnestly implemented more proactive and effective macroeconomic policies. They have risen to the occasion, responded calmly, and worked tirelessly to foster sustained economic recovery and growth, firmly advancing high-quality development. Meanwhile, macro-control measures have been strengthened, with monetary policy remaining moderately accommodative—continuously delivering targeted support while fine-tuning efforts at appropriate moments—to bolster counter-cyclical adjustments. A range of monetary policy tools have been deployed comprehensively, ensuring that financial resources are channeled effectively into the real economy, thereby creating an ideal monetary and financial environment for economic rebound and improvement. At the same time, it is crucial to enhance the flexibility, precision, and effectiveness of monetary policy management. Policymakers must closely monitor both domestic and global economic and financial conditions as well as market dynamics, carefully calibrating the intensity and timing of policy implementation. This includes rigorously executing all monetary policy measures to fully unlock their intended impact. Moreover, maintaining ample liquidity remains essential, guiding financial institutions to boost lending and credit expansion. This will ensure that the growth rates of total social financing and money supply align closely with projected targets for economic growth and overall price levels. Additionally, structural monetary policy tools should be effectively deployed, supporting key areas such as technological innovation, consumer spending, small and micro enterprises, and stable foreign trade. Special attention should also be given to critical sectors like "dual priorities" and "new initiatives," providing robust financing support where needed. Efforts should focus on accelerating the implementation of already-announced financial policies and measures, while simultaneously boosting efforts to revitalize existing housing stock and underutilized land resources. These actions will help stabilize the real estate market, strengthen its foundation, and ultimately contribute to the establishment of a new model for real estate development. Finally, it is vital to strike a balanced approach between aggregate supply and demand, enhancing coordination among macroeconomic policies. By upholding policy continuity and stability, while building in greater flexibility and forward-thinking, we can further expand domestic demand, anchor market expectations, and unleash economic vitality, thereby solidifying and broadening the momentum of the ongoing economic recovery and growth.

Currently, the traditional "Golden September and Silver October" peak season for the steel market this year is already nearing its end. Downstream terminal demand has been weaker than market expectations, though significant support from various sources of capital continues to flow into major projects. However, given the ongoing drag from the real estate sector, the recovery in construction steel demand during the peak season remains limited. As a result, the market continues to operate under the clear logic of "looking at reality during the peak season." Meanwhile, "trade frictions" between China and the U.S. have reignited recently. Amidst growing external uncertainties, market participants still hold certain policy expectations ahead of the upcoming 4th Plenary Session of the 20th Central Committee. Consequently, the steel market is likely to shift back to its usual "anticipating trends during the off-season" operating pattern. (Lange Steel Research Center, Ge Xin, 15810671409 [WeChat ID also available]; please credit the source when reprinting.)

2025-12-08

2025-12-01

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com