2024-12-03

"At the end of the year," steel companies' profits may improve.

In October, the operating conditions of China's steel industry improved, and the industry's loss margin narrowed. According to data from the National Bureau of Statistics, from January to October 2024, the black metal smelting and rolling processing industry achieved operating revenue of 648.913 billion yuan, a year-on-year decrease of 6.4%; operating costs were 625.709 billion yuan, a year-on-year decrease of 5.8%; and losses amounted to 23.32 billion yuan, a year-on-year decrease of 183.6%. In October alone, the black metal smelting and rolling processing industry made a profit of 10.78 billion yuan, turning losses into profits and reducing the overall loss scale of the industry.

The main reason for the steel industry's turnaround in October was the strong expectations released by macro policies, which led to steel prices entering a high-level adjustment period in October, with the monthly average price significantly rising, while the monthly average price of raw materials increased only slightly. Additionally, steel mills had previously stored raw materials at relatively low prices, resulting in a noticeable improvement in the operating conditions of steel companies in October. In November, the steel market continued to adjust and weaken, with raw material prices fluctuating slightly at high levels, and the profitability of steel companies significantly weakened compared to October. It is expected that the profit data released for the steel industry in November will show a month-on-month decline.

Looking ahead to December, the steel industry will enter a seasonal demand off-peak period. How will the operating conditions of steel companies evolve at the end of the year? The Lange Steel Research Center believes that profitability in the steel industry may improve in December.

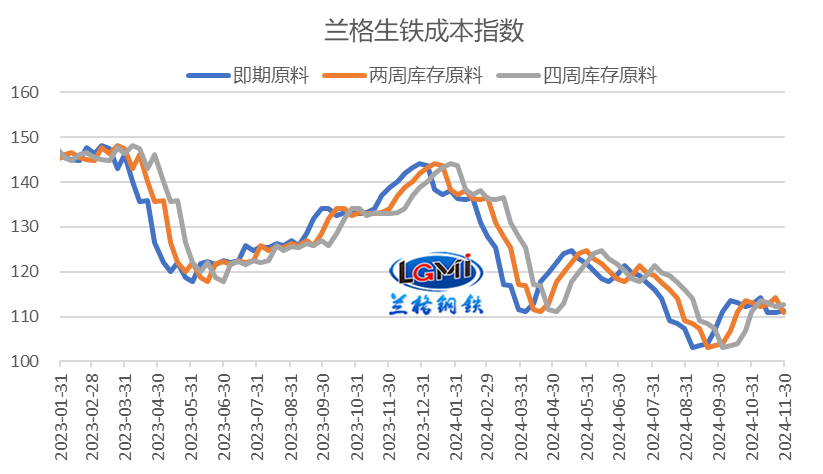

In November, with the fluctuation of major raw materials at high levels, the monthly average cost level remained high, and the spot costs slightly decreased, while the monthly average costs calculated from two-week and four-week inventory raw materials significantly increased. Monitoring data from the Lange Steel Research Center shows that the iron cost index for spot raw materials in November 2024 was 111.8, a decrease of 0.7% compared to the same period last month; the iron cost index for two-week inventory raw materials was 112.5, an increase of 2.5% compared to the same period last month; and the iron cost index for four-week inventory raw materials was 112.9, an increase of 6.8% compared to the same period last month.

Figure 1: Lange Iron Cost Index Trend Chart

From a cyclical perspective, as steel prices fluctuated downward in November, the profitability of various products deteriorated. On average, in November, the Lange Steel Comprehensive Steel Price Index had a monthly average of 3749 yuan (per ton), a decrease of 3.6% compared to the previous month; among them, the monthly average price of rebar was 3513 yuan, down 6.8% from the previous month; and the monthly average price of hot-rolled sheets was 3615 yuan, down 1.2% from the previous month. Compared to costs, the decline in spot costs in November was weaker than the decline in steel prices, while the monthly average cost calculated from two-week and four-week inventory raw materials increased by 2.5% to 6.8%, leading to a deterioration in the profitability of steel companies.

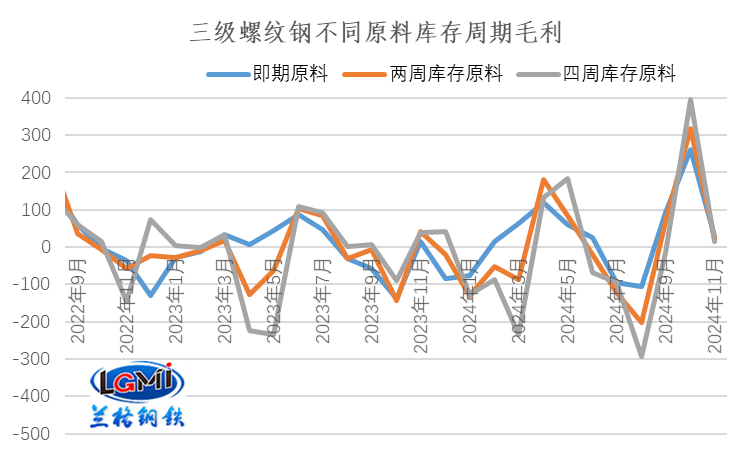

For grade three rebar, the monthly average gross profit calculated from spot raw materials, two-week inventory raw materials, and four-week inventory raw materials in November was 28 yuan, 23 yuan, and 16 yuan, respectively, decreasing by 233 yuan, 294 yuan, and 380 yuan compared to the previous month, indicating a significant narrowing of profit margins (see Figure 2).

For hot-rolled sheets, the calculated loss from spot raw materials in November was 34 yuan, an increase in loss of 15 yuan compared to the previous month. The monthly average losses calculated from two-week and four-week inventory raw materials were 40 yuan and 46 yuan, respectively, both turning from profit to loss.

Figure 2: Changes in Gross Profit Levels of Grade Three Rebar with Different Inventory Cycles

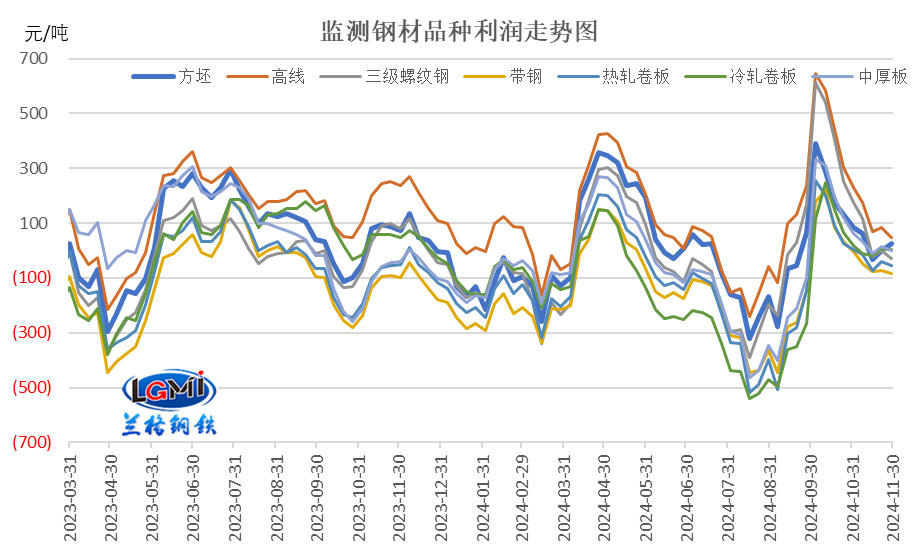

In terms of gross profit performance calculated from four-week inventory raw materials, the gross profit of various products in November showed a low-level fluctuation trend, with monthly average profits significantly declining. Monitoring data from the Lange Steel Research Center shows that among the seven major products monitored, the monthly average profits of strip steel, hot-rolled sheets, and cold-rolled sheets were in a loss state, with losses ranging from 5 to 70 yuan; other products still had certain profits, with profit margins ranging from 8 to 93 yuan, significantly narrowing compared to the previous month.

Figure 3: Gross Profit Levels of Major Steel Products (Four-Week Inventory Raw Materials)

Overall, under the combined influence of high-level price declines for various products and the relative resilience of average raw material prices, the calculated gross profit per ton of steel from spot, two-week, and four-week inventory raw materials all deteriorated in November. It is expected that the monthly profit of steel companies in November 2024 will shrink significantly.

In December, the global manufacturing PMI showed a steady recovery within the contraction range, and the global economy maintained a weak and stable recovery trend. The expectation of further interest rate cuts by the Federal Reserve remains strong, which is beneficial for supporting commodity prices. However, factors such as geopolitical conflicts, trade frictions, and high debt levels continue to be uncertainties hindering the recovery of the global economy.

From a domestic perspective, on November 8, the Standing Committee of the National People's Congress approved an increase of 6 trillion yuan in the local government debt limit to replace existing hidden debts. The state is promoting the resolution of large-scale hidden debts, which helps local governments reduce their burdens and free up resources to promote development and benefit people's livelihoods. In mid-December, the Central Economic Work Conference will be held, and it is expected that in response to external shocks, the macro policy orientation for 2025 will continue to maintain a positive attitude. In the next stage, the state will strengthen macroeconomic regulation, effectively utilize various policy tools, expand domestic demand, enhance innovation-driven growth, and consolidate the positive momentum of economic recovery.

From the supply side, in November, the profitability of steel companies shrank, but some products still had certain profits, which kept the production willingness of steel companies strong. It is expected that domestic steel production in November may continue to show a slight rebound. According to estimates from the Lange Steel Research Center, the national daily crude steel output in November may rise to around 2.7 million tons. In December, crude steel production may shrink month-on-month, but year-on-year growth may still be maintained due to the low base from the same period last year.

From the demand side, the steel market will enter a traditional demand off-peak season in December, and the demand for construction steel will gradually shrink. The manufacturing sector's prosperity continues to recover, with both the production index and new orders index rising within the expansion range. It is expected that the demand for steel in manufacturing in December will be steadily released.

From the cost side, in November, raw material prices fluctuated within a range, and the monthly average production costs of steel slightly decreased, with costs still providing resilience to steel prices.

From the market trend perspective, as global economic uncertainties increase, market expectations for domestic policies have strengthened. With the arrival of the off-peak season, the supply-demand relationship in the market will tend to loosen, but currently, costs still provide resilience to steel prices. The intensity of policy implementation and the scale of winter storage will be key driving factors for market trends in December. The Lange Steel Big Data AI-assisted decision-making system predicts that the domestic steel market may show a fluctuating and slightly strong operating trend in December 2024.

In terms of steel company profitability, under the fluctuating and slightly strong operating trend of the steel market in December, combined with the relatively loose supply-demand relationship on the raw material side, the overall upward space is limited. The Lange Steel Research Center expects that profitability for steel companies may improve in December.

Previous Page

Previous Page

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com