2025-06-16

Steel mills' profit margins may narrow in June.

From January to April 2025, driven by the continuous release of China's steady growth and incremental policies, cost reductions, and the boost to production and sales from export competition, the profits of steel industry enterprises continued to improve. Data from the National Bureau of Statistics shows that from January to April 2025, the ferrous metal smelting and pressing and processing industry achieved an operating revenue of 2483.66 billion yuan, a year-on-year decrease of 6.5%; operating costs were 2370.64 billion yuan, a year-on-year decrease of 8.3%; and total profits were 16.92 billion yuan.

In May, with the "temporary suspension" of the US-China tariff war, the implementation of China's loose monetary policy, and the implementation of interest rate cuts and reserve requirement ratio reductions, the domestic steel market still showed an overall fluctuating downward trend due to factors such as the gradual shift of demand towards the off-season and the relatively high level of supply. Costs remained relatively resilient, and the profitability of the steel industry narrowed, but profits are still expected. Looking ahead to June, the steel industry will enter the off-season for demand, and the demand for construction steel will continue to shrink. Will steel companies be able to maintain their operating conditions? Lange Steel Research Center believes that the steel industry's operations may be under pressure in June 2025.

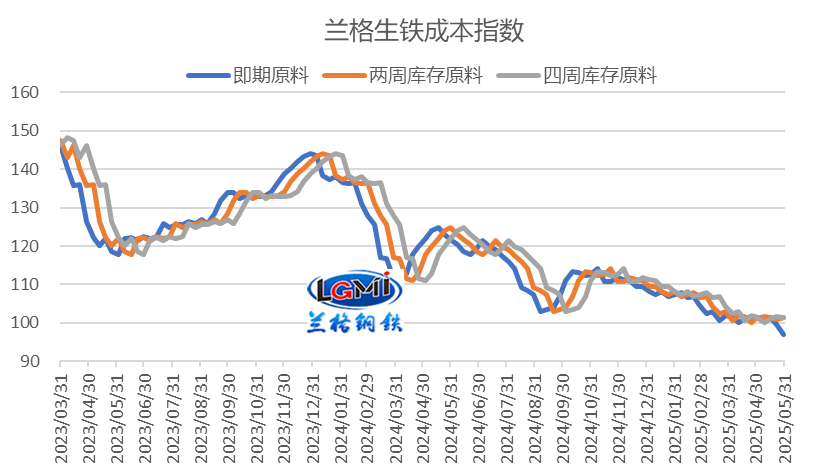

In May 2025, the stable raw material prices in the early period and the significant drop in iron ore prices at the end of the month led to different changes in the average monthly cost. The average monthly cost calculated using spot and four-week inventory raw materials both fell, while the average monthly cost calculated using two-week inventory raw materials remained resilient. Lange Steel Research Center's monitoring data shows that in May, the spot raw material-based pig iron cost index was 99.6, down 1.5% year-on-year; the two-week inventory raw material-based pig iron cost index was 101.3, up 0.2% year-on-year; and the four-week inventory raw material-based pig iron cost index was 101.1, down 0.9% year-on-year.

Figure 1 Lange Pig Iron Cost Index Trend Chart

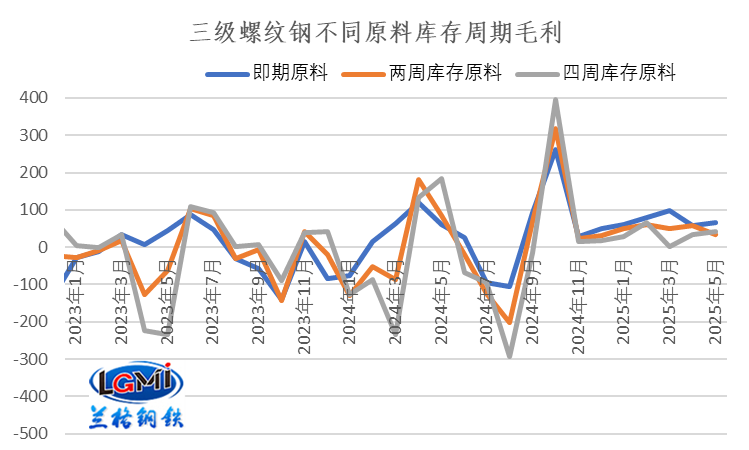

In terms of the average steel price, the Lange Steel Comprehensive Steel Price Index averaged 3531 yuan/ton in May, down 1.1% month-on-month; among them, the monthly average price of rebar was 3308 yuan, down 0.5% month-on-month; and the monthly average price of hot-rolled coils was 3366 yuan, down 0.9% month-on-month. From a cyclical perspective, costs in May showed some differentiation due to changes in raw material inventory cycles, and profitability also showed some differentiation.

Looking at Grade III rebar, the average monthly gross profit calculated using spot raw materials, two-week inventory raw materials, and four-week inventory raw materials in May were 66 yuan, 35 yuan, and 41 yuan, respectively. Compared to the previous month, these increased by 8 yuan, decreased by 22 yuan, and increased by 8 yuan, respectively. This shows that under the spot and four-week raw material cycles, cost reductions led to a slight improvement in profitability, while under the two-week raw material inventory cycle, costs remained resilient, and profits deteriorated under the condition of falling prices in the variety material market (see Figure 2 for details).

Looking at hot-rolled coils, the calculated gross profit in May also showed some differentiation. The loss calculated using spot raw materials was 18 yuan, unchanged from the previous month; the average monthly loss calculated using two-week inventory raw materials was 48 yuan, an increase of 28 yuan compared to the previous month; and the average monthly loss calculated using four-week inventory raw materials was 43 yuan, a decrease of 1 yuan compared to the previous month.

Figure 2 Changes in the Gross Profit Level of Grade III Rebar Calculated Using Raw Materials with Different Inventory Cycles

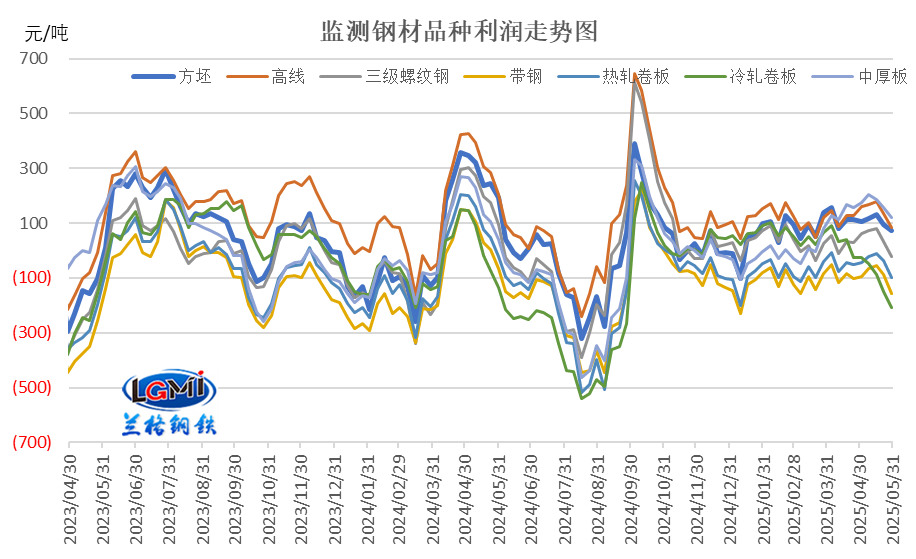

Looking at the gross profit performance of various products calculated using four-week inventory raw materials, the gross profit of various products calculated using four-week inventory raw materials in May showed a trend of rising first and then falling, except for billets and cold-rolled coils, whose profits decreased slightly; Lange Steel Research Center's monitoring data shows that among the seven major products monitored, the gross profit of medium and thick plates improved the most, reaching 19 yuan; the gross profit improvement of other products ranged from 1 to 12 yuan; the gross profit of billets decreased by 11 yuan compared to the previous month; and the gross profit of cold-rolled coils decreased by 146 yuan compared to the previous month, turning from profit to loss.

Figure 3 Gross Profit Level of Major Steel Products (Four-Week Inventory Raw Materials)

In general, under the combined influence of the continued decline in the prices of various steel products and the downward trend in production costs, the per-ton gross profit of various steel products calculated using spot, two-week, and four-week inventory raw materials in May showed some differentiation. The profitability of spot and four-week inventory raw materials improved, while the profitability of two-week inventory raw materials deteriorated; it is expected that the steel company profit data officially released in May will still be relatively good.

The situation facing the steel industry in June remains complex and changeable. From the perspective of the international environment, the global manufacturing PMI continues to decline, and the global economic outlook has significantly deteriorated. Tariff increases and uncertainty in trade policies put pressure on supply chains, pushing up production costs, leading to slower investment by businesses, and affecting both developed and developing economies.

From the perspective of the domestic environment, China currently faces many external instabilities and uncertainties, and the foundation for the continued recovery and improvement of the national economy still needs to be further consolidated. China will adhere to the general work guideline of pursuing progress while maintaining stability, accelerate the construction of a new development pattern, coordinate domestic economic work and international trade disputes, focus on stabilizing employment, enterprises, markets, and expectations, and promote the continued recovery and improvement of the economy.

From the supply side of the steel industry, the "temporary suspension" of the US-China tariff war and the implementation of interest rate cuts and reserve requirement ratio reductions have temporarily alleviated the "external pressure" since the beginning of the year, and the effect of the domestic "incremental policies" will gradually become apparent, effectively stabilizing the market during the upcoming traditional off-season for demand. It is expected that domestic steel production in May will remain high. According to Lange Steel Research Center's estimates, China's daily crude steel production in May will remain at around 2.9 million tons. In June, with slowing demand and weak profitability, crude steel production is expected to decline.

From the demand side, in June, high temperatures and heavy rainfall will gradually increase, inhibiting the construction of construction projects and further slowing down the demand for construction steel. The demand for steel in the manufacturing industry will maintain a certain resilience, but some industries will also be under pressure.

From the cost side, the average price of raw materials fell in May, and the average monthly steel production cost decreased slightly, and the support of costs for steel prices continued to weaken.

In summary, the domestic steel market in June will still be affected by multiple factors. External instabilities and uncertainties remain high, and the foundation for the continued recovery and improvement of the national economy still needs to be further consolidated; while the increase in high-intensity rainfall across the country in June will further slow down the demand for construction steel, and social steel inventories may rebound from the bottom, exacerbating the supply-demand contradiction. Coupled with the further weakening of cost support, Lange Steel's big data AI-assisted decision-making system predicts that the domestic steel market in June 2025 may show a weak bottoming-out trend.

From the perspective of steel company profits, under the weak bottoming-out trend of the steel market in June 2025, Lange Steel Research Center predicts that the operating profits of steel companies in June may face the risk of further narrowing. (Original article by Wang Guoqing of Lange Steel Research Center, please indicate the source when reprinting)

Hotline:4000-91-9898

Copyright © 2024 Tianjin Youfa Steel Pipe Group Co., Ltd.

State Internet Information Office Reporting Center Tianjin Internet Illegal and Bad Information Reporting Center Reporting E-mail:yfmarket@yfgg.com

National Hotline:4000-91-9898

Copyright © 2024

Tianjin Youfa Steel Pipe Group Co., Ltd. All Rights Reserved

National Internet Information Office Reporting Center

Tianjin Internet Illegal and Bad Information Reporting Center

Reporting E-mail:ppclglzx@aimatech.com